Authority Brands Taps ChargeAfter to Power BuyFin, Enabling Frictionless Financing for Homeowners Read more>>

X

Author: chargeafterdev

“ChargeAfter is amongst our top rung of partnerships, and they enable us to deliver consistent. The conversion uplifts ChargeAfter creates helps drive strong value for DXL Group and our customers.”

ChargeAfter has been nominated as a USA finalist in the 2023 Banking Tech Awards. The nomination demonstrates the company’s commitment to innovation and excellence in fintech. As we look forward to the winner’s ceremony on June 1, 2023, we eagerly anticipate the outcome and the opportunity to celebrate the outstanding achievements and successes of ChargeAfter and its fellow nominees.

The yearly Banking Tech Awards USA celebrates remarkable accomplishments and triumphs in the American banking and fintech sector. The United States hosts numerous prominent global financial service centers and experiences rapid growth in the financial technology market. These awards honor the exceptional achievements and successes of the nation’s most talented individuals and innovative businesses.

ChargeAfter has been nominated as a USA finalist in the prestigious 2023 Banking Tech Awards this year. The company is a finalist for ‘Best Embedded Finance System – Lending’ award – a testament to its exceptional work in fintech. With their innovative embedded lending platform, ChargeAfter has made significant strides in the industry, offering businesses a seamless and efficient way to offer any type of consumer financing.

The 2023 Banking Tech Awards, presented by FinTech Futures, is the top international source of unbiased intelligence and expertise for professionals within the fintech industry. The awards highlight the rapid growth and cutting-edge developments in the financial technology market by showcasing the best and brightest in the field.

The winner ceremony will occur at the luxurious 583 Park Avenue in New York City on June 1, 2023. This event will bring together leaders, innovators, and visionaries from the banking and fintech sectors to celebrate their achievements and successes. It promises to be an unforgettable night filled with networking opportunities, inspiring speeches, and the recognition of outstanding accomplishments.

To join the celebration and witness the crowning of the winners, bookings can be made at https://informaconnect.com/banking-tech-awards-usa/purchase/select-package/. Take the opportunity to participate in this exciting event, where you can connect with industry professionals, learn about the latest trends in fintech, and celebrate the triumphs of the best in the business.

The consumer credit market has evolved significantly, from its limited offline beginnings to the emergence of point-of-sale financing and Buy Now Pay Later (BNPL) options. These developments have provided consumers with greater choice and flexibility. However, limitations in lending offerings at the point of sale – in-store and online – can still restrict consumer options and hinder merchant sales. This is where ChargeAfter comes in, connecting lenders and consumers at any point of sale, offering a seamless solution akin to how Visa and MasterCard operate in the payment space. In this podcast, Meidad Sharon, the founder and CEO of ChargeAfter, explores the evolution of the credit market and how ChargeAfter addresses the limitations in the current market.

The Evolution of the Credit Market:

In the podcast, Meidad Sharon discusses how the credit market has evolved from a limited, offline solution to one with point-of-sale financing and Buy Now Pay Later (BNPL) options, offering consumers more choice and flexibility. However, he points out how current lenders tend to focus on specific financial products, credit segments, and territories, limiting consumer options and hindering merchant sale conversions.

ChargeAfter’s Solution:

ChargeAfter aims to address these limitations by easily connecting multiple lenders and consumers at the merchant’s point of sale, online and in-store, providing a seamless solution similar to how Visa and MasterCard connect the payment space. With ChargeAfter, merchants can access multiple lenders in a single integration, covering the full credit spectrum and offering various financing solutions for B2C and B2B customers. This approach aims to optimize financing options, increase sale conversions, and create a more connected consumer credit market.

Support Each Lender Unique Underwriting Model:

ChargeAfter presents lending options to consumers based on each lender’s unique underwriting model, which considers various data points beyond credit scores. Consumers can then choose the best fit for their preferences from the available credit options, allowing them to find the most suitable financial solution.

Future of the Credit Market:

The market now recognizes that BNPL and point-of-sale financing are here to stay and will likely be the future of consumer credit. Consumers are likely to expect all their credit options to be available instantly at the point of sale. Major payment players have adopted consumer finance, including BNPL, within the last 18 to 24 months, merging the previously separate payments and point-of-sale financing markets. This trend indicates that BNPL and point-of-sale financing will become a standard offering alongside credit cards and alternative methods like PayPal.

ChargeAfter’s Role in Enabling Regulation:

As the BNPL market matures, regulation is essential to protect consumers from over-borrowing and to ensure transparent disclosures. ChargeAfter, as the platform embedding lenders and BNPL providers at the point of sale, plays a significant role in enabling this regulation by connecting merchants to regulated and trusted lenders while providing the best solution to consumers.

Demand from Banks to Enter or Expand Their Presence in POS Financing:

There is a growing demand from banks to enter or expand their presence in the POS financing and BNPL market. They have provided credit for many years and are eager to expand their offering at the point of need with multiple consumer financing products.

ChargeAfter supports banks and financial institutions by embedding them in the merchant’s customer journey, shopping carts, and checkout experiences through white-label BNPL & consumer finance solutions, allowing banks to offer financing to their consumers without being a tech expert or a customer experience expert.

Sector-Specific Differences in Financing:

Point of sale financing and BNPL vary across different sectors. In industries with high average order values, such as healthcare, home improvement, furniture, and electronics, financing is crucial for consumers, accounting for up to 80% of sales. In other industries, financing accounts for 10%-50% of sales, it is on the rise.

ChargeAfter’s Vision for the Future of the BNPL Market:

ChargeAfter has a big vision for the future of the BNPL market, anticipating more lenders, financing products, and more consumer financing options. They see new forms of financing emerging to cater to changing consumer preferences, like renting items instead of long-term ownership. As consumer demand increases and the number of solutions are on the rise – the need for an embedded lending platform for POS financing becomes inherent to omnichannel customer journeys, simplifying the consumer financing process end to end.

Financing data will become increasingly important to merchants, lenders, and financial institutions, enabling them to optimize their offerings and gain better visibility into consumer behavior. ChargeAfter provides control, connectivity, and real-time matching between consumers, transactions, and lenders while addressing data security and compliance challenges for banks and merchants.

Conclusion:

The consumer credit market has undergone significant changes, and point-of-sale financing and BNPL options have emerged as key players. ChargeAfter is an innovative solution that connects lenders and consumers at the point-of-sale, offering a seamless and optimized financing option for B2C and B2B customers. Its unique technology simplifies complex underwriting, regulations, and compliance needs. Its data-driven approach allows its partners to maximize the benefits of offering point-of-sale financing. The future of the BNPL market looks bright, and ChargeAfter has a big vision to expand its platform by adding more lenders, financing options, and countries. The credit market continually evolves, and ChargeAfter is well-positioned to create a more connected credit market.

Take advantage of valuable insights into the evolution of the credit market and how ChargeAfter is changing the game with point-of-sale financing and BNPL options. Listen to the podcast featuring Meidad Sharon, the founder and CEO of ChargeAfter, now to learn more!

Over the past few years, many retailers have concentrated on direct-to-consumer and e-commerce. As part of this – specific consideration has been given to consumer financing, and significant agreements have been made between consumer finance FinTech companies and big-brand companies such as Walmart, United Airlines, Amazon, Lenovo, and many others, even though these retailers already have well-established private label credit card programs.

Consumer appetite for consumer financing and BNPL drives merchant demand for point-of-sale financing.

Beyond surveys, historical growth statistics, or forecasts for rising popularity in consumer finance, the evidence lies with two simple metrics:

— How many companies include consumer financing at their point of sale, and — Are any big brand retailers are embracing it

The fact is, consumer financing has always been a staple with big retailers.

The difference in recent times is that big brands recognize the benefits of partnering with innovative FinTechs, allowing them to concentrate on their core business while benefiting from new technologies as they are developed.

Previously, this was exclusive to merchants with the resources to integrate or develop point-of-sale finance options into their platform.

Innovation by FinTechs has accelerated the adoption of consumer finance as demand by merchants is fueled by consumers’ need for affordability in the face of the current and imminent challenging financial environment.

It is essential to understand that consumer finance does not exclusively mean Buy Now Pay Later (BNPL), although BNPL does fall under the umbrella of consumer finance.

Evolution of consumer finance

Consumer financing has evolved from credit cards and prime lending solutions often offered by traditional financial institutions such as banks to a technology-diverse fintech landscape with various financial service providers and platforms.

But what does this new ‘landscape’ offer, and how do we navigate it?

We look at how merchants use various consumer finance options and highlight their benefits.

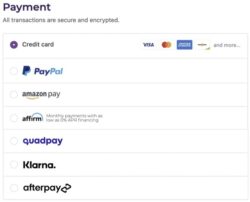

Credit Card

The credit card option at checkout is widely known to us. It is the most prevalent payment method. Almost all banks and financial institutions provide many credit card types that are accepted as payment methods offering goods or services anywhere. One can purchase anything within a predetermined credit limit and pay later without impacting their monthly budget. A key advantage of using a credit card is converting the total purchase amount into affordable equated monthly installments (EMI), facilitating easy repayment over time. EMI conversions from credit card purchases have transformed the shopping experience significantly.

As popular as credit cards have been, consumers know their glaring disadvantages. The most infamous being high-interest charges. Further, the prime lender provides the loan (credit). i.e., the institution that issued the credit card reduces the credit limit by an amount equal to the bill amount converted into EMIs.

Buy Now, Pay Later

Single Lender BNPL Platform

BNPL (Buy Now, Pay Later) is unsecured consumer credit and an increasingly popular fintech-enabled payment option, most commonly offered on e-commerce platforms. The history of BNPL traces back to the installment plan – a way to pay for large purchases over time by spreading it over several smaller payments.

As a form of POS (point-of-sale) financing, credit originates directly at the time and point-of-sale, as opposed to a customer being required to secure credit from a lender ahead of their shopping experience.

Fintech companies have developed different flavors of BNPL. However, most are similar in that they have a single lender. Sometimes, as with PayPal, the lender is also the technology provider.

Studies have shown that BNPL increases retail sales. The reason is that some consumers may not have a credit card, prefer not to use credit cards, and many times look at BNPL as a better alternative to credit card installments, as BNPL offers an alternative to installment payments that is often with favorable repayment terms when compared to the use of credit cards.

Most, if not all, well-known big brands, such as Amazon, Walmart, and many more, have teamed up with BNPL FinTechs to expand their consumer financing options to increase sales while limiting risk. This strategy has proved to be successful.

Walmart

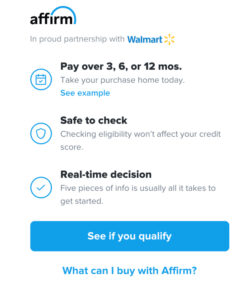

Walmart is an American multinational retail corporation that operates a chain of hypermarkets, discount department stores, and grocery stores. With over 10,000 stores in 27 countries, Walmart offers a wide range of products, including groceries, electronics, clothing, and home goods, at low prices to attract budget-conscious shoppers. The company is known for its efficient supply chain management. Walmart added Affirm as a BNPL for installments of 3,6 and 12 months.

Amazon

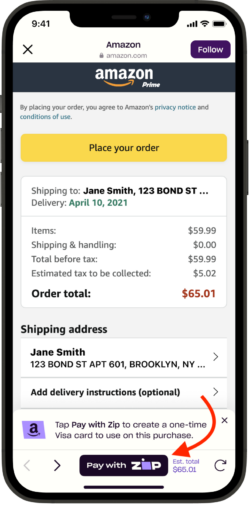

The largest retailer in the world and founded in 1994, Amazon is a multinational technology company. It specializes in e-commerce, cloud computing, digital streaming, and artificial intelligence.

In this example , Amazon has partnered with ZIP to offer short terms installments.

The problem with single-lender BNPL

However, although very convenient, single-lender BNPL platforms do not necessarily offer the consumer the best loan terms and are limited to BNPL only.

Customers must conform to single-lenders’ terms of service and credit score policy.

Imposing these terms of service may result in less than desired loan terms offered to the consumer or, even worse, a failed loan origination. Both scenarios heighten the probability of sale abandonment.

Big brands have recognized that consumers shop for the best deals, not only in products and services but also in costs and terms associated with financing their purchases.

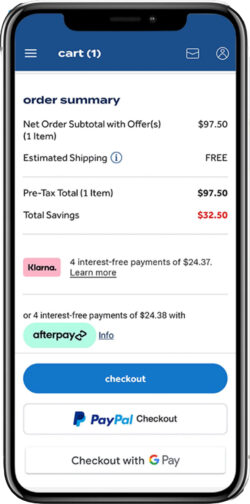

For this reason, established merchants offer customers multiple payment options at checkout. Including multiple BNPL service providers and options. Most of which are single-lender platforms.

Bed Bath & Beyond, for instance, diversifies its consumer financing options to its customers by partnering with multiple BNPL financing providers. Merchants have found that sale abandonment decreased because customers have more options for lending at the point-of-sale. While this is a good strategy by the merchants, it has many limitations. For one, it is still a limited short-term installment offering. Even when using several BNPLs, surveys found that almost 30% of merchants report that their consumer financing approval rates are less than 60%.

Furthermore – it creates a fragmented checkout experience. Sometimes, customers may still abandon their cart, feeling overwhelmed, unsure, and confused with the various options. Decision paralysis occurs because there is too much choice.

A study by SMARTASSISTANT found that 54% of consumers have stopped purchasing products from a brand or retailer website because choosing was too difficult.

The same is true for products & services and checkout payment options alike.

Multi-lender Consumer finance & BNPL platforms

As a means to offer the advantages of the different types of consumer finance options available and address their shortcomings, ChargeAfter developed a multi-lender consumer finance embedded lending platform.

Backed by over 40 lenders, in a single checkout financing option, merchants can offer their customers the best consumer loan at checkout, which is lightning fast and provides the best loan terms.

ChargeAfter’s platform and network finds the best loan suited for the customer and merchant with a streamlined and efficient process that feels indigenous to the merchants’ site and brand.

Unlike conventional consumer finance options and single-lender BNPL, surveys have shown that multi-lender consumer finance platforms achieve loan approvals of 80% or more.

ChargeAfter’s platform is seamlessly integrated throughout the merchants’ channels – online and in-store – to create an omnichannel experience that feels proprietary to the consumer. The benefit of omnichannel experience in itself adds value to the merchant.

As a solution that maximizes return through its obsession with the customer journey experience, ChargeAfter’s platform elevates the consumer experience, reduces cart abandonment, and increases return business.

Some examples of big brands using a multi-lender platform include:

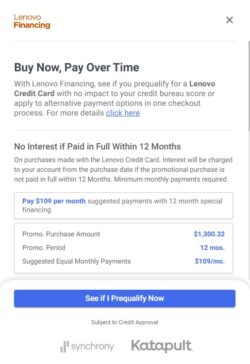

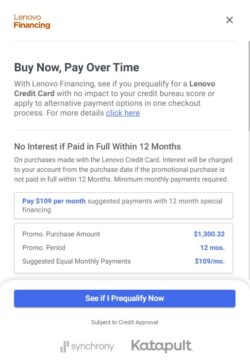

Lenovo

Founded in 1984 and specializing in personal computers, smartphones, tablets, and other electronic devices, Lenovo is the world’s largest PC vendor by unit sales.

Lenovo is a multinational technology company that operates in over 60 countries.

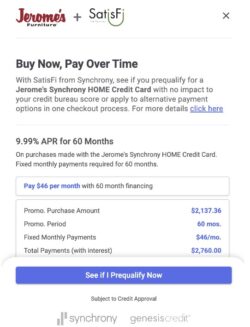

Jerome’s Jerome’s Furniture is a family-owned and operated retailer that has been serving Southern California for over 65 years.

About ChargeAfter

ChargeAfter is the leading multi-lender white-labeled consumer financing platform and lender network for global banks, financial institutions, and merchants. Powered by a data-driven decision engine and network of international lenders, ChargeAfter streamlines the distribution of credit into a single platform that merchants can implement rapidly online, in-store, and across any point of the loan.

ChargeAfter investors include The Phoenix, Citi Ventures, Banco Bradesco, Visa, MUFG, BBVA, Synchrony Financial, PICO Venture Partners, Propel Venture Partners, and Plug and Play VC. ChargeAfter is headquartered in New York.

For more information, visit: https://chargeafter.com/about/.

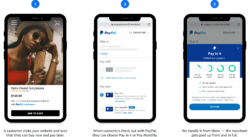

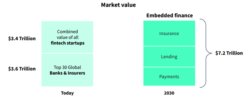

Embedded finance is a growing trend in the finance industry that involves integrating financial services into non-financial customer journeys, and it is now becoming prevalent in both B2C and B2B contexts. Embedded finance options will eventually be the norm for B2C purchases, even for traditionally conducted offline transactions. This trend helps to increase customer engagement and loyalty. As this trend continues to grow, many industries are exploring various embedded finance use cases.

What is Embedded Finance?

Embedded finance allows non-financial companies to integrate financial services or products into their digital offerings, making it more convenient for customers to purchase products and streamlining business processes. This trend has also led to embedded fintech, wherein financial service platforms integrate into commercial or financial service platforms.

In short, an embedded finance ecosystem integrates the various spheres necessary to complete the entire cycle of a financed transaction.

For instance, when a retail customer makes a purchase (in-store or online) and opts to pay for the purchase in installments, three things need to exist;

The Seller – The merchant selling the product or services through the systems they employ. In this case their Point-Of-Sale system.

In embedded finance, this is the ‘Distributor’ or ‘Embedder.’

These are retailers, software companies, and marketplaces – that integrate financial services into their products to benefit their customers.

The Lender – providing finance for the product or services purchased in point #1 for a fee and/or interest, allowing the seller to sell a product with no financial risk.

However, sometimes the ‘lender’ role is also fulfilled by the seller as a second source of revenue by offering loans with interest.

This is the ‘Balance Sheet Provider’ or ‘Financial service provider’: Banks, fintech, and other financial institutions.

And

Technology Provider – configuring and integrating the systems between the seller system and the lender system to create and maintain a seamless transaction

The ‘Technology Provider’ or ‘embedded financing platforms‘ are both experts in the seller technologies and service design and well-versed in the regulations and intricacies of providing financial services. They help stitch the embedded finance ecosystem together. They look at the customer journey to provide processes that are simplified and personalized.

A real world example would be Point of Sales financing whereby:

The retailer would be the ‘Seller’ such as Lenovo

The ‘Balance Sheet Provider’ would be a group of lenders bidding to offer the best consumer financing deal (long term installments financing)

The ‘Technology Provider’, such as ChargeAfter’, enables this transaction to occur by integrating and connecting ‘The seller’ with ‘the balance sheet provider’ in an automated manner, facilitating the transaction efficiently.

Types of Embedded Finance

* Embedded finance, a multi-trillion dollar opportunity, Source: The rise of embedded finance, Dealroom and ABN AMRO Ventures, 2022

Embedded Lending and Buy Now Pay Later (BNPL)

BNPL is an example of embedded lending. It falls under Point of Sale financing (also known as POS financing). BNPL is a lending option that allows customers to purchase goods or services and pay for them through short term installment loans. BNPL financing is usually offered by fintech companies.

Point-of-sale (POS) financing is an umbrella term that describes a variety of embedded lending methods and products. These include BNPL but also pay over time for longer and bigger purchases, as well as 0% APR, revolving line of credit, lease-to-own, and more.

Point-of-sale loans like these are gaining popularity and have become essential in improving the user experience and driving customer loyalty through repeat purchases.

According to a 2022 article by The Ascent, 56% of consumers surveyed in 2021 have used a buy now, pay later service, this is up from 37% in July 2020*

Increasingly, Point-of-sale loans are integrated with online e-commerce websites as well as in-store.

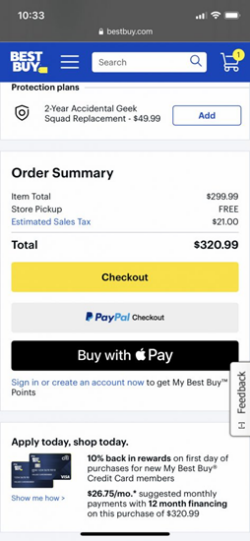

Well-known big retail brands such as Best Buy, Costco,, Target, Walmart, and countless others recognize the value in offering various embedded consumer finance options in their online channels and stores with an omnichannel experience. Many of these big brands opt to integrate with consumer financing platforms such as ChargeAfter instead of developing their own.

ChargeAfter’s omnichannel multi-lender platform is designed to support merchants by providing various financing options to consumers and businesses. The platform is pre-integrated with more than 30 leading lenders, enabling merchants to offer multiple financing options using a single application directly on their e-commerce website or retail location. The platform allows for a quick financing approval process, with up to 85% of financing approvals completed in less than three seconds.

ChargeAfter’s embedded financing platform is designed to offer shoppers various financing options, regardless of their credit history. The platform offers 0% APR, open lines of credit, short and long-term installments, card installments, lease-to-own, and B2B financing options.

There are many examples of well-known retail brands that offer embedded financing and BNPL at the point of sale. Below are some examples:

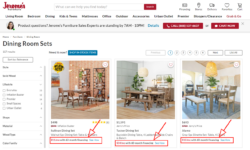

Jerome’s Furniture:

showcases its financing options already at the homepage, allowing customers to prequalify for financing offers.

In addition they embed the financing offer within the PDP:

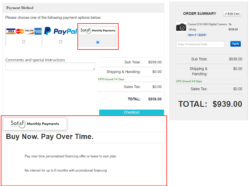

42photo.com

Presents a promo pop up with the financial offer – welcoming any customer to to choose business financing

embedding the Point of Sale financing as part of a seamless checkout process:

Digital Wallets Integrated into Mobile or Online Platforms

Digital wallets allow customers to store and use digital currency to make payments or transfers, manage their financial accounts and track their spending. They can also be linked to traditional bank accounts or credit cards, providing a seamless and convenient way to make transactions. Examples of digital wallets include Apple Pay and Google Wallet.

Some of Apple’s partners, to name but a few, include Best Buy, Disney, Dunkin Donuts, McDonald’s, Walgreens, Costco, Target, and Taco Bell.

Google Pay also facilitates payment with Best Buy and other distributors.

Loyalty programs with digital or store credit rewardsLoyalty programs that offer rewards or cashback in the form of digital currency or store credit allow customers to earn and use rewards or cashback within the platform or service they are already using. For example, credit card companies or retailers may offer rewards or cashback through loyalty points redeemed for discounts or other benefits.A familiar example of a loyalty program is the Star Bucks Rewards.

Conclusion

Embedded finance has arrived and is making its way into the finance ecosystem. The trend will continue to grow throughout all verticals of business and service providers, and more industries will adapt to it. By integrating financial services or products into their platforms, merchants can offer a more seamless customer experience while streamlining their back-end processes. With the advent of omnichannel lending, including POS financing and BNPL, the future of B2C and B2B financing at the point of sales looks bright.

The rapidly evolving retail financing landscape presents new growth opportunities for merchants looking to expand their businesses.

Providing an omnichannel experience for consumer financing options is becoming increasingly important. With implementing a consumer financing platform a priority, it is crucial to manage the financing cycle and integrate with in-store point-of-sale systems. In this article, we will outline key points based on ChargeAfters’ Retailer Survey on the State of Consumer Financing related to retail financing and the implications for merchants in 2023.

What is in the Survey

Explore a range of retailer priorities on consumer finance, including:

Demand for Consumer Financing

Find out the importance of consumer financing and retailers’ take on consumer demand for POS financing.

Consumer Finance Approval Rate

In the survey, we assess the frequency of customers who walk away with a poor customer experience and lost revenues for the business and how statistics are a problem for near-prime and subprime customers.

Merchants find this information critical for expanding their financing options to remain competitive. Learn about the importance of Retail financing options such as in-store financing, checkout finance, and payment plans and how these can help merchants offer financing solutions that meet the needs of their customers.

Demand for Expanding Consumer Finance Lenders

Retailers want to serve the entire credit spectrum better and add to their lender portfolio. See how important it is for retailers to add B2B lenders, tertiary lenders (also known as a third-look lender), and secondary lenders to their financing portfolio.

The survey reveals how the drive to broaden the variety of options for consumers translates directly to improving the customer experience and revenues for the merchants, who are currently leaving money on the table.

Importance of Implementing Consumer Finance

End-to-end management of the financial cycle is crucial for financing platforms. Retailer insights reveal retailer priority on implementing a consumer financing platform and the range of essential considerations required, like, how the platform should manage the financing cycle, from reconciliations to chargebacks and dispute resolution, the ability to integrate with in-store Point-of-Sale, offering an omnichannel experience and connectivity to various lenders.

How vital is Consumer Experience & Omnichannel?

Providing omnichannel financing options is vital for most merchants, but smaller merchants must catch up. Today’s consumers often require an omnichannel experience when utilizing consumer financing and BNPL tools. The survey shows the importance of consumer experience and omnichannel from the retailer’s perspective.

The data paints a picture of consumer finance as an increasingly critical function in the business, linked to customer experience, revenues, and business growth. With technology investments and expansion a priority, merchants ask themselves – am I remaining competitive enough to support the business and my customers?

Conclusion

Download the FREE survey to gain insight into retailers’ demand for consumer financing, particularly for lower-priced items.

Find out what retailers need to improve customer experience and revenue and how crucial it is for merchants to provide an omnichannel experience for financing options. In the survey, learn how consumer financing is becoming an integral part of the customer experience, with some retailers creating a unique function for BNPL and consumer financing options.

As technology investments and expansion become a priority for merchants in 2023, they must remain competitive enough to support their businesses and customers. By understanding and addressing these critical findings in our survey, You can see how merchants can leverage the advantages of financing and capitalize on the growth opportunities offered by the rapidly evolving retail financing landscape.

Visit us at eTails Retail Conference held at JW Marriott Desert Springs in Palm Springs, California. The event is running from 27 February 2023 to 2 March 2023.

You will find our booth at ‘Startup Valley’

ChargeAfter is a b2b FinTech omnichannel innovator of Consumer Finance. We offer flexible white-label financing solutions for retailers and online merchants.

Our consumer financing solutions enable you to offer finance wherever your shoppers are. Online, In-store, and over the phone.

eTail has been bringing together global brands and retailers since 2003 and is excited to continue gathering key industry players in a safe, collaborative, and personalized way. The event is for senior-level, omnichannel & e-commerce executives and buyers who look to remain innovative and ahead of the curve by delivering value.

The event offers access to over 1800 retail professionals, of which over 53% are Director/VP level and up, making it a valuable investment of time. eTail is a must-attend for leading e-commerce and omnichannel minds and brings together a high proportion of decision-making teams with buying power

The event consolidates leading experts in retail to share knowledge and insights on the latest industry disruptions and future trends. With a 65% retailer attendance rate, it is the only event in the industry that has more buyers in attendance than sellers.

Furniture industry research specialist Dana French conducted the Consumer Insights Now research, which was released in September and was co-sponsored by ChargeAfter. The consumer finance study highlights customer behaviors across age groups (18-74). The primary goal of the research was to identify customer preferences and trends which would provide furniture sellers with useful information.

The survey provides data on how buyers often use consumer financing in a variety of ways. The research’s results include the kinds of goods they want to purchase, how they intend to finance such purchases, and how the furniture fits into their overall shopping list.

The research gives furniture retailers all the information they need to know about customer trends right now. For both new and established retailers looking to offer the precise services that customers want, the data may be of tremendous assistance. Especially when the study displays a variety of consumer behavior statistics.

The study emphasizes once more how essential consumer financing has become to our daily lives and how it affects every significant purchase made by a customer. Numerous survey results show that younger customers are more inclined to utilize consumer financing in their everyday life which is evidence that retail finance has become popular in recent years.

The survey’s findings could help retailers understand the value of customer financing in the furniture industry. It may be a signal for them to introduce additional buy-now, pay-later (BNPL) loans or POS financing alternatives.

The results of the survey also revealed which age group is the most significant group of consumers and which of them must be the primary category of potential customers. As a result, the data may be used by retailers to create a precise marketing strategy for upcoming sales and ensure that customers will have access to the financing choices they require. When properly applied, research may boost sales and conversion rates for shops.

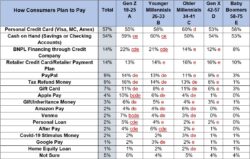

How Consumers Plan To Pay

According to the chart above, different age groups have different plans for how they will make their payments, or use consumer finance solutions. Although the numbers for customers who use credit cards and those who prefer to pay with cash are practically identical, we can see that younger groups are slightly biased towards cash payments. Due to their familiarity with traditional banking services and installment payments, older generations are more inclined to utilize credit cards for payment.

In contrast, younger Millennials and Gen Z tend to choose Buy Now Pay Later services from financing platforms when it comes down to consumer financing options available to them.. There are two potential causes for this. Namely, younger consumers may like BNPL since it offers superior services and the benefit, occasionally, of no interest charges, or are often unable to qualify for credit cards because they do not yet have a solid credit score. Similar considerations apply to cash payments, which are often made from savings accounts and are more frequently made by older generations.

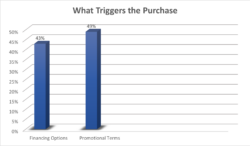

Are Consumer Financing Options And Promotional Terms Important To Consumers?

Promotional terms are significant to 49% of customers overall for home goods, whereas financing options are important to 43% of customers when we compare how financing choices and promotions trigger the purchase for the consumers. The younger generations of Gen Z are the only age group, as shown in the table above, that is more likely to make a purchase when the shop offers financing choices at the point of sale. However, this is not true for other age groups. Only 27% of Baby Boomers believe that financing alternatives at the store are the reason to make a purchase, according to the lowest numbers for consumer finance.

Though the comparison is close across practically all age groups, younger generations are more influenced by both possibilities and are more likely to purchase as a result. As we can see, promotional conditions are an excellent instrument for boosting sales and luring customers. Conversely, the businesses that choose to use both of the proposed solutions will succeed the most and draw in the most number of customers.

As shown, the Consumer Insights Now consumer finance survey provides the exact data and facts furniture retailers require to develop effective new tactics and know which consumer financing solutions to use.

References:

Consumer Insights Now research, Home News Now (September 11, 2022) Consumer Insights Now: Research highlights consumer buying behavior in the second half

Consumers are increasingly turning to Buy Now Pay Later (BNPL) or POS financing to purchase items or services and spread out their payments over time with a preset payment plan.

A recent poll found that during the COVID-19 outbreak, 60% of participants used a buy now, pay later service. 66 percent of respondents stated that they believe adopting buy now, pay later services to be “financially dangerous” at the same time. This is probably because services that let customers purchase items now and pay for them later might lead to overspending. Services that let you buy now and pay later may give the impression that an item is less expensive than it is. If shoppers indulge themselves, they could accumulate more credit than they can manage.

Important Data for BNPL

In 2022, there are expected to be 59.3 million BNPL users. The amount of BNPL customers has been sharply rising over time, driven in part by the financial difficulties associated with COVID and in part by the proliferation of BNPL businesses.

This line of credit is adaptable and simple to qualify for. For example, 45% of customers said they picked BNPL because paying with it was simpler than using a credit card, while 44% claim they did so because it offers more flexibility.

BNPL Use by Age

Age

BNPL User Percentage

18-24

61%

25-34

60%

35-44

61%

45-54

53%

54+

41%

BNPL Use by Average Household Income

Average Household Income

BNPL User Percentage

>$35,000

39%

$35,000-$49,999

47%

$50,000=$74,999

50%

$75,000-$99.999

43%

>$100,000

41%

People between the ages of 18 and 24 and 35 to 44 are the most likely to finance BNPLs. In general, younger age groups utilize BNPL more frequently. The income range of $50,000–74,999 is the one most probably to use BNPL. Customers in this range and those above it utilize BNP at around the same rates.

According to the most recent statistics, BNPL loan usage decreases as income and age rise. However, the trend suggests that this pattern is changing, and more and more individuals are beginning to use BNPL lending, which is hurting traditional banking products.

Top Reasons for BNPL Usage

Reasons to Use BNPL

Percentage of Users

Out of Budget Purchase

44.98%

Avoiding CC Interest

36.92%

Borrow Money

24.73%

Avoiding to Share Personal Data

20.79%

Credit Card Alternative

19.18%

Reached Credit Card Limit

17.2%

Can’t get CC

14.16%

No Bank Account

7.71%

Other

5.73%

Generally, purchasing clothing and electronics is the most frequent usage of a BNPL plan. The most frequent reason for selecting a BNPL plan is to make an expensive purchase.

Amounts People Owe to BNPL

Amount owed

User Percentage

Less than 100

28%

101-250

18%

251-500

25%

501-1000

17%

1001-2500

9%

2501-5000

2%

More than 5000

1%

BNPL Companies

Not just businesses and consumers benefit from BNPL loans; BNPL service providers also make significant profits. Even if the majority of the top financing platforms don’t charge consumers any additional fees, they nevertheless make money from the merchant companies that use their services to run their online storefronts. Simply defined, BNPL services are simple to use, but difficult to produce and secure. As a result, rather than developing a new system on their own, retailers employ the established and reliable financing systems of BNPL companies to increase their sales and conversion rates. Additionally, it draws a lot more customers overall.

Instead of just employing basic BNPL services, merchants and retailers are increasingly turning to the newly created and deployed BNPL white label services. Retailers can adopt BNPL services and do so under their name by using ChargeAfter’s white-label services. They get considerably better outcomes from branded BNPL solutions, which also improves the reputation and overall attractiveness of their business.

ChargeAfter’s BNPL Financing Platform

ChargeAfter’s Waterfall financing increases the chance of approval — up to 85%.

Additionally, ChargeAfter is constantly improving and working to provide its merchants and banking partners with the best and most up-to-date services. According to Meidad Sharon, CEO of ChargeAfter, in an interview with Fintech Blueprints, the system is updated at least montly, and by the end of this year, they intend to increase the number of lenders to further ensure that every customer can get the financing they need.