Unleash the Power of Embedded Finance: Here Are Some Use Cases

Introduction

Embedded finance is a growing trend in the finance industry that involves integrating financial services into non-financial customer journeys, and it is now becoming prevalent in both B2C and B2B contexts. Embedded finance options will eventually be the norm for B2C purchases, even for traditionally conducted offline transactions. This trend helps to increase customer engagement and loyalty. As this trend continues to grow, many industries are exploring various embedded finance use cases.

What is Embedded Finance?

Embedded finance allows non-financial companies to integrate financial services or products into their digital offerings, making it more convenient for customers to purchase products and streamlining business processes. This trend has also led to embedded fintech, wherein financial service platforms integrate into commercial or financial service platforms.

In short, an embedded finance ecosystem integrates the various spheres necessary to complete the entire cycle of a financed transaction.

For instance, when a retail customer makes a purchase (in-store or online) and opts to pay for the purchase in installments, three things need to exist;

The Seller – The merchant selling the product or services through the systems they employ. In this case their Point-Of-Sale system.

In embedded finance, this is the ‘Distributor’ or ‘Embedder.’

These are retailers, software companies, and marketplaces – that integrate financial services into their products to benefit their customers.

The Lender – providing finance for the product or services purchased in point #1 for a fee and/or interest, allowing the seller to sell a product with no financial risk.

However, sometimes the ‘lender’ role is also fulfilled by the seller as a second source of revenue by offering loans with interest.

This is the ‘Balance Sheet Provider’ or ‘Financial service provider’: Banks, fintech, and other financial institutions.

And

Technology Provider – configuring and integrating the systems between the seller system and the lender system to create and maintain a seamless transaction

The ‘Technology Provider’ or ‘embedded financing platforms‘ are both experts in the seller technologies and service design and well-versed in the regulations and intricacies of providing financial services. They help stitch the embedded finance ecosystem together. They look at the customer journey to provide processes that are simplified and personalized.

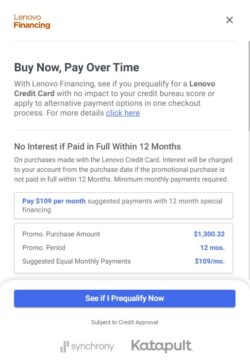

A real world example would be Point of Sales financing whereby:

- The retailer would be the ‘Seller’ such as Lenovo

- The ‘Balance Sheet Provider’ would be a group of lenders bidding to offer the best consumer financing deal (long term installments financing)

- The ‘Technology Provider’, such as ChargeAfter’, enables this transaction to occur by integrating and connecting ‘The seller’ with ‘the balance sheet provider’ in an automated manner, facilitating the transaction efficiently.

Types of Embedded Finance

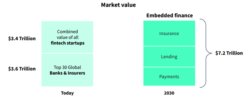

* Embedded finance, a multi-trillion dollar opportunity, Source: The rise of embedded finance, Dealroom and ABN AMRO Ventures, 2022

-

Embedded Lending and Buy Now Pay Later (BNPL)

BNPL is an example of embedded lending. It falls under Point of Sale financing (also known as POS financing). BNPL is a lending option that allows customers to purchase goods or services and pay for them through short term installment loans. BNPL financing is usually offered by fintech companies.

Point-of-sale (POS) financing is an umbrella term that describes a variety of embedded lending methods and products. These include BNPL but also pay over time for longer and bigger purchases, as well as 0% APR, revolving line of credit, lease-to-own, and more.

Point-of-sale loans like these are gaining popularity and have become essential in improving the user experience and driving customer loyalty through repeat purchases.

According to a 2022 article by The Ascent, 56% of consumers surveyed in 2021 have used a buy now, pay later service, this is up from 37% in July 2020*

* https://www.fool.com/the-ascent/research/buy-now-pay-later-statistics/

Increasingly, Point-of-sale loans are integrated with online e-commerce websites as well as in-store.

Well-known big retail brands such as Best Buy, Costco,, Target, Walmart, and countless others recognize the value in offering various embedded consumer finance options in their online channels and stores with an omnichannel experience. Many of these big brands opt to integrate with consumer financing platforms such as ChargeAfter instead of developing their own.

ChargeAfter’s omnichannel multi-lender platform is designed to support merchants by providing various financing options to consumers and businesses. The platform is pre-integrated with more than 30 leading lenders, enabling merchants to offer multiple financing options using a single application directly on their e-commerce website or retail location. The platform allows for a quick financing approval process, with up to 85% of financing approvals completed in less than three seconds.

ChargeAfter’s embedded financing platform is designed to offer shoppers various financing options, regardless of their credit history. The platform offers 0% APR, open lines of credit, short and long-term installments, card installments, lease-to-own, and B2B financing options.

There are many examples of well-known retail brands that offer embedded financing and BNPL at the point of sale. Below are some examples:

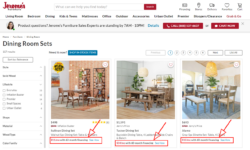

Jerome’s Furniture:

showcases its financing options already at the homepage, allowing customers to prequalify for financing offers.

In addition they embed the financing offer within the PDP:

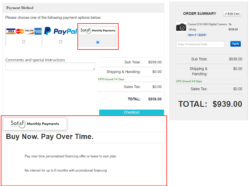

42photo.com

Presents a promo pop up with the financial offer – welcoming any customer to to choose business financing

embedding the Point of Sale financing as part of a seamless checkout process:

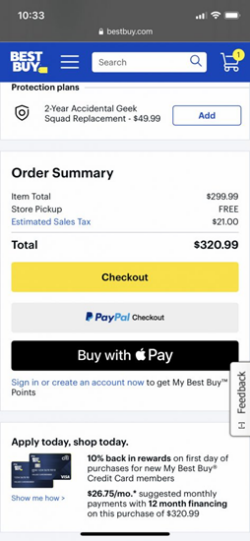

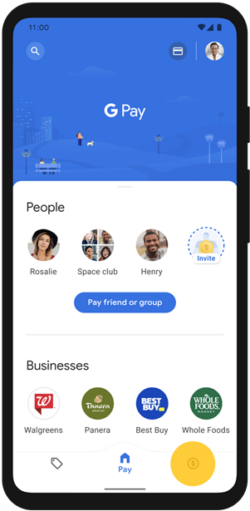

Digital Wallets Integrated into Mobile or Online Platforms

Digital wallets allow customers to store and use digital currency to make payments or transfers, manage their financial accounts and track their spending. They can also be linked to traditional bank accounts or credit cards, providing a seamless and convenient way to make transactions. Examples of digital wallets include Apple Pay and Google Wallet.

- Some of Apple’s partners, to name but a few, include Best Buy, Disney, Dunkin Donuts, McDonald’s, Walgreens, Costco, Target, and Taco Bell.

- Google Pay also facilitates payment with Best Buy and other distributors.

- Loyalty programs with digital or store credit rewardsLoyalty programs that offer rewards or cashback in the form of digital currency or store credit allow customers to earn and use rewards or cashback within the platform or service they are already using. For example, credit card companies or retailers may offer rewards or cashback through loyalty points redeemed for discounts or other benefits.A familiar example of a loyalty program is the Star Bucks Rewards.

Conclusion

Embedded finance has arrived and is making its way into the finance ecosystem. The trend will continue to grow throughout all verticals of business and service providers, and more industries will adapt to it. By integrating financial services or products into their platforms, merchants can offer a more seamless customer experience while streamlining their back-end processes. With the advent of omnichannel lending, including POS financing and BNPL, the future of B2C and B2B financing at the point of sales looks bright.