Point-of-sale financing is evolving to play a strategic role for merchants that contributes to improved sales conversion and customer loyalty. The prequalification process presents the perfect opportunity for retailers to convert browsers into buyers. By simplifying the process, retailers establish a foundation for customer loyalty which in turn can lead to long-term business growth.

To leverage the potential of point of sale financing, leading merchants are increasingly opting for a multiple lender platform-first approach. In addition to meeting customer needs, its back office capabilities make it easier for merchants to manage the end to end process while offering lender redundancy, greater control, and financing data and analytics.

At ChargeAfter, the embedded lending platform for point-of-sale financing, we are dedicated to optimizing performance to help merchants that harness our platform better serve their customers and improve the bottom line.

The importance of checkout optimization

The ChargeAfter checkout team is dedicated to designing and implementing a user experience that maximizes conversion rates. By refining and optimizing the prequalification process for point-of-sale financing, the team aims to encourage more customers to complete their purchases. “More applications mean more opportunities for customers to make a purchase,” Anna Peters, Director of Product, Consumer Experience explains, highlighting the direct link between the checkout experience and sales performance.

Experimentation: the key to continuous improvement

The primary goal of the team is to increase conversion rates or, at the very least, ensure that any changes do not negatively impact these rates or the customer experience. The approach to experimenting with the checkout process is meticulous and data-driven. “Deciding on an experiment is a very thoughtful process,” explains Anna. The team starts by clearly defining the challenge they aim to solve, formulating hypotheses, and identifying supportive data. Then, they outline the metrics needed to measure impact, plan the design, development, and rollout phases, and finally, conduct the experiment.

These experiments are crucial for making informed decisions, allowing ChargeAfter to move beyond opinions and rely on actual user data. This approach has led to significant improvements, with some experiments yielding a conversion rate increase of 5% to 12%.

Challenges and solutions in experimentation

The path to optimization is not without its challenges. Interpreting results and managing internal expectations can be complex tasks. The team addresses these challenges by maintaining clear communication and setting realistic expectations based on data and previous outcomes.

The impact of experiments

The experiments conducted by ChargeAfter have had a tangible positive impact on both the customer experience and merchant Key Performance Indicators (KPIs). For instance, one experiment tested whether starting the flow without an overview screen of how ChargeAfter’s product works could affect application submissions. The result was a remarkable 12% increase in submissions.

Another set of experiments focused on the impact of improved messaging and visuals regarding the no credit score impact feature on various screens throughout the checkout process. While the overall change in conversion was neutral across all merchants, this was seen as a positive outcome since there was no degradation in conversion rates. Moreover, some individual merchants saw increases, with one furniture merchant experiencing a 4% rise in conversion, indicating a successful adjustment to a new, more effective baseline.

The role of merchant involvement

Merchant involvement is crucial in shaping these experiments. According to Anna, partners are not only supportive but eagerly anticipate the results of these tests. This collaborative approach ensures that experiments are aligned with merchants’ goals and customer needs, leading to mutually beneficial outcomes.

Conclusion: a collaborative path to improvement

These experiments highlight the power of data-driven experimentation in optimizing the checkout experience. By focusing on the user experience and continuously testing and refining their approach, ChargeAfter is helping merchants increase conversion rates and, ultimately, sales. These efforts underscore the importance of embracing innovation and collaboration to meet the ever-changing demands of consumers and the marketplace.

About Varda Bachrach Varda has over 20 years of experience in marketing, content, and communications, most recently in fintech start ups where she loves simplifying complex messages.

The prevalence of Buy Now, Pay Later (BNPL) schemes has been remarkable in recent years, capturing the attention of more than half of U.S. consumers, according to data from Bankrate. However, despite the popularity of this type of loan, BNPL is decreasing in popularity and is only one of many point-of-sale financing options.

In this article we explore BNPL and explain how it is only one element of the broader consumer financing market.

What is Buy Now, Pay Later (BNPL)?

Buy Now, Pay Later (BNPL) revolutionizes the purchasing process by allowing consumers to defer the full payment for goods and services. Through this innovative payment model, shoppers can instantly finance their acquisitions, repaying the amount in fixed, interest-free installments over a predetermined time frame. For example, a purchase worth $100 could be divided into four installments of $25 each.

This financing solution has seen widespread adoption across various business sectors, especially among e-commerce retailers, for its ability to significantly uplift conversion rates, augment average order values, and broaden customer bases. At the end of 2022, retailers offering BNPL options reported up to a 30% increase in sales volume, according to an article in PYMNTS, attesting to the method’s effectiveness in enhancing sales performance while offering customers the flexibility of staggered payments.

The Rising Popularity of Buy Now, Pay Later

Buy Now, Pay Later (BNPL) services have surged in popularity, with 50 million consumers in the United States adopting this flexible payment option over the past year, according to PYMNTS research. This trend reflects a growing consumer appetite for manageable payment plans and signals a significant opportunity for merchants, as nearly 60% of consumers are aware of BNPL. Implementing BNPL options can increase sale likelihood by 20% to 30% and raise the average transaction size by up to 50%, translating into considerable revenue boosts for retailers. Additionally, a recent survey highlighted that nearly 70% of customers spend more when using BNPL services, further encouraging merchant adoption. This financial model benefits businesses by driving sales, increasing ticket sizes, and promoting financial inclusion among diverse groups, including recent immigrants, by making essential services more accessible. Despite the consistent use of BNPL among U.S. shoppers since 2021, interest in future use has grown, indicating an expanding market. The advantages for merchants are clear: offering BNPL can significantly enhance customer spending behavior and loyalty, underscoring the importance of overcoming any implementation challenges to capitalize on this lucrative trend.

How do Buy-Now-Pay-Later Services Work?

BNPL services facilitate a streamlined shopping experience, enabling loan application at checkout, available for both online and in-store purchases. The approval process from the BNPL platform is swift, leading to an immediate initiation of the repayment plan with an upfront payment at purchase. The ensuing installments are designed to be interest-free, with additional fees applied only in instances of delayed payments.

How Buy-Now-Pay-Later Services Make Money

BNPL platforms derive revenue from two primary sources: merchants and consumers. The merchant fees might include an initial setup cost and a per-transaction charge, whereas consumer fees generally entail penalties for late payments. This dual-income model supports the operational viability of BNPL services, offering interest-free installment plans to shoppers.

What Are The Benefits Of Buy-Now-Pay-Later Services?

BNPL services streamline the checkout process, offering a seamless and personalized payment experience that caters to customer preferences. These benefits extend beyond convenience, as BNPL options also improve conversion rates, and elevate average order values.

Challenges with Providing Buy-Now-Pay-Later Options

Despite the advantages, BNPL solutions have their limitations, particularly concerning credit inclusivity and the financing of larger purchases. The existing one-size-fits-all approach of many BNPL providers fails to accommodate the diverse financial needs of all consumers, potentially leading to higher default rates and financial strain for those unable to meet repayment obligations. Further, BNPL providers face new regulations and legislations in 2024 which could challenge their existing models.

Consumer Financing Platforms

Distinguishing themselves from BNPL services, consumer financing platforms offer more flexibility.. These platforms, by connecting with multiple lenders, are able to tailor financial solutions to individual consumer needs more effectively, making them a preferable choice for merchants and their customers. Lenders also benefit from this model which connects them to suitable borrowers at their moment of need, creating a win-win-win situation.

BNPL vs. Consumer Finance

There are a number of fundamental differences between the Buy Now Pay Later scheme (BNPL) and traditional consumer finance which affect the choice of consumers and investment behavior. The first difference is the simplicity of BNPL because there is no interest on short-term purchases, which means that for those people who would like to make smaller payments without paying extra costs, this can be an ideal option. Consequently, due to these factors, BNPL has become very popular with less expensive items that can be easily repaid over a shorter period of time.

Unlike BNPL services, which usually charge no interest, traditional consumer finance—credit cards and personal loans usually involve interest rates and sometimes additional fees; however, it provides more freedom when choosing an amount of the loan as well as its repayment duration. So, in this case, it is more preferable for major purchases or consolidation of debt over the longer time horizon. The credit check required by the banks before granting such type of credit is a barrier for some consumers who have had earlier problems with repayment but also a benefit ensuring that they will not be burdened with further financial obligations beyond their means.

When deciding between BNPL and consumer finance, consumers’ financial health as well as their liquidity are of much concern. The zero-interest installment options provided by BNPL might be pocket-friendly when one needs to make an urgent purchase, but the possibility of higher credit limits and a longer repayment period on consumer finance acts as a safety net for bigger financial requirements or unforeseen contingencies. In order to choose between BNPL and traditional consumer finance, consumers must consider their financial standing along with fiscal stability in the long term, weigh immediacy versus flexibility, and assess growth possibilities in terms of larger credit lines.

Selecting the ideal BNPL provider necessitates an assessment of factors such as repayment terms, credit limits, and customer demographics. Providers differ in their offerings, for example:

Affirm: provides installment plans ranging from short-term options to loans extendable up to 36 months, with varying APRs based on the purchase and customer creditworthiness.

Afterpay: (Clearpay in the UK and EU) offers four interest-free payments, catering to users in multiple regions with its expansive user base.

Klarna: introduces flexibility with payment plans that spread the cost over several months or allow for deferred payments, in addition to offering financing options for longer periods.

An embedded lending platform, such as ChargeAfter’s, ensuring a broad range of consumer finance options beyond BNPL, including revolving credit, short and long-term loans, private label credit cards, lease-to-own, and B2b options, catering to diverse consumer needs and enhancing approval rates.

Selecting the Right POS Financing Solution

In choosing a POS financing solution , merchants should consider factors such as repayment terms, credit limits, and geographical reach to ensure alignment with their product offerings and customer demographics. Platforms like ChargeAfter simplify this selection process by providing access to a multi-lender network that offer competitive terms, enabling merchants to seamlessly add or remove lenders from their points of sale, and deliver a multi-lender waterfall financing experience that boosts approval rates to up to 85%.

Integration and Support Across Platforms

ChargeAfter enables easy integration of financing options at omnichannel points of sale, ensuring merchants can offer diverse financing solutions effortlessly. The platform also provides robust post-sale management tools, facilitating efficient transaction oversight and customer service and actionable insights to optimize the lending offer and convert more sales.

For businesses aiming to maintain brand consistency, the platform offers white-label financing solutions that allow merchants to customize the financing experience to align with their brand identity, enhancing customer recognition and trust.

In consumer finance, the methods we use to pay for goods and services are significantly transforming. Innovative financing solutions challenge traditional payment methods like cash and credit cards, reshaping consumer spending habits and preferences. This shift not only influences how consumers choose to pay for goods and services but also offers new opportunities for merchants to enhance their sales strategies. Let’s explore the evolving trends in cash, credit card use, and the burgeoning field of point-of-sale (POS) financing.

Cash: The Decline of Transactions

The journey towards a cashless society has accelerated, driven by the advent of mobile and digital wallets. Despite the United States trailing behind countries like the United Kingdom, Norway, China, and Canada regarding digital payment adoption, a notable decline in cash usage is evident. Federal Reserve data highlights that cash accounts for only 20% of transactions in the U.S., predominantly for small purchases with an average value of $22. The trend away from cash is becoming more pronounced. Pew Research Center noted a significant increase in Americans who report not using cash for purchases in a typical week, jumping from 24% in 2015 to 41% in 2023.

Credit Cards: A Waning Popularity

Credit cards, once the cornerstone of unsecured borrowing in the U.S., are witnessing a dip in popularity, especially among younger generations. GlobalData’s 2023 research revealed decreased credit card ownership among Americans under 35. This shift is partly attributed to the stringent borrowing conditions, exemplified by a 20% loan rejection rate reported by the Federal Reserve in July 2023, following multiple interest rate hikes. The search for alternatives is driven by the high average credit card APR, which stands at nearly 25%, pushing consumers to seek more favorable financing options.

POS Financing: The Emergence

The development of POS financing technology has introduced many financing products into the market, revolutionizing consumer financing at checkout. This sector, predominantly spearheaded by fintech innovations, offers a range of loans, including 0% APR, diverse installment plans, and B2B financing solutions. ChargeAfter’s data underscores a significant uptick in consumer spending through financing, with a 53% increase in the first quarter of 2023 compared to the previous year. The allure of POS financing lies in its ability to provide immediate, flexible financing options, often with more favorable terms than traditional credit cards.

Consumer Financing: the Future Landscape

Consumer financing is veering towards POS solutions as younger consumers move away from credit cards. The evolving financial technology landscape heralds a future where consumer financing is increasingly integrated into the shopping experience, offering seamless and versatile financial solutions.

While cash offers simplicity and debt-free transactions, it is overshadowed by the convenience and benefits of digital payments. Despite their flexibility, credit cards are becoming less favorable due to the potential for high-interest debt. In contrast, POS financing platforms that support a multitude of lenders and integrate seamlessly into omnichannel retail environments are rapidly gaining traction among merchants eager to offer their customers a breadth of financing options.

In conclusion, the dynamics of consumer payments are shifting dramatically, with POS financing emerging as a critical player in the retail sector. As technology continues to evolve, the potential for innovative consumer financing solutions promises to reshape the financial landscape, offering consumers more control over their spending while providing merchants with powerful tools to boost sales and customer satisfaction.

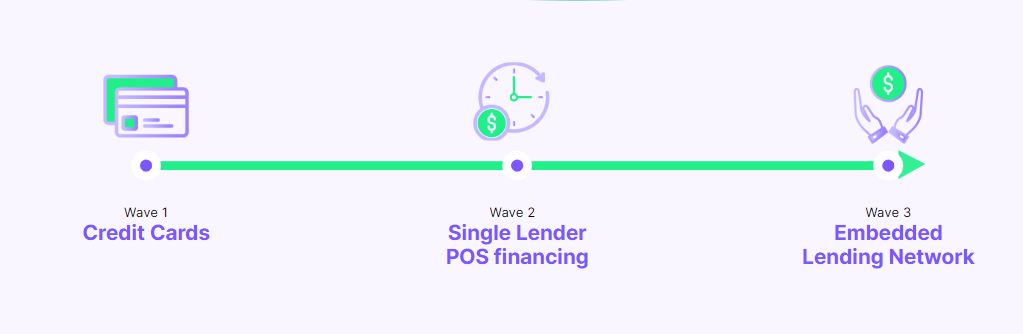

In recent years, POS financing has emerged as a game changer, enabling merchants to meet the demand for flexible financing solutions embedded within the purchasing journey. This growing demand is a result of multiple factors, including the emergence of new fintech lenders that have entered the market with competitive terms, a challenging economy for consumers, and younger Americans rejecting credit cards.

This next wave of credit not only enhances consumers’ purchasing power but also opens new strategic avenues for merchants to increase sales and foster customer loyalty. With various POS financing solutions available, understanding and integrating suitable options can significantly impact your sales strategy.

What is POS financing?

POS financing, or point-of-sale financing, refers to lending options available to customers at their moment of need in the purchasing process. Unlike traditional financing, which often involves lengthy application processes and extensive paperwork, POS lending offers instant loan approvals directly at checkout, bridging the gap between customer desire and purchase capability.

Types of POS Financing

The landscape of POS financing is diverse, offering several tailored options to meet the varied needs of businesses and consumers. POS financing covers different types of lending products that cover the full credit spectrum. Merchants that want to provide their customers with a robust POS financing experience embed different types of financing options into their points of sale to increase approval rates to up to 85%.

0% APR Financing

0% APR programs allow customers to make purchases without incurring any interest during a specified period making them an appealing financing option. Consumers can buy a product immediately and pay back the cost over time, but unlike traditional loans, they are not charged any interest, provided the repayment is completed within the agreed timeframe. This type of financing is particularly beneficial for purchasing big ticket items, as it makes them more financially accessible and manageable for the consumer. Retailers often use 0% APR offers as an incentive to encourage higher sales and attract budget-conscious customers, enhancing both the affordability of their products and the attractiveness of their sales proposition. By offering a cost-effective way to spread out payments, 0% APR loans at the point of sale can significantly improve the purchasing power of consumers, while simultaneously driving business growth and customer loyalty.

Consumer BNPL (Buy Now, Pay Later)

Buy Now, Pay Later (BNPL) is a flexible payment solution that has revolutionized the retail industry in recent years. BNPL allows consumers to divide the total purchase price into smaller, more manageable installments, often with the initial payment due at the time of purchase and the rest spread over a short period. The key appeal of BNPL lies in its accessibility and convenience: customers can acquire goods immediately, from everyday items to more substantial purchases, without the upfront financial burden. This method is especially attractive for those who need or want products immediately but prefer not to exhaust their savings or use traditional credit options. For retailers, offering BNPL can significantly boost sales, attract a broader customer base, and improve customer satisfaction by providing a flexible and customer-friendly payment alternative. By aligning with modern spending habits and offering immediate gratification with delayed payment, BNPL is a powerful tool for enhancing both consumer purchasing power and business growth.

Business BNPL

B2B financing, tailored specifically for business-to-business transactions, plays a crucial role in smoothing the financial interactions between companies. This form of financing addresses the unique needs of businesses, offering them more flexible payment terms and credit options for purchasing goods or services. B2B financing often involves larger purchases and repayment periods ranging from 30 days to 12 months or more. It is designed to enhance cash flow management for both buyers and sellers, enabling businesses to maintain operational efficiency without the immediate financial strain of large purchases. This can be particularly beneficial for smaller businesses that may not have extensive capital reserves. By facilitating easier and more manageable trade, B2B financing strengthens business relationships, fosters long-term collaboration, and supports the overall growth and stability of the business ecosystem. For companies looking to invest in equipment, inventory, or services to expand their operations, B2B financing offers a vital resource to achieve these goals without disrupting their financial health.

Lease-to-Own

Lease-to-own is an innovative payment solution that blends elements of leasing and purchasing, offering consumers and businesses a flexible pathway to ownership. This option allows customers to lease a product—often electronics, furniture, or appliances—for a set period, with the opportunity to purchase the item at the end of the lease term. During the leasing period, customers make regular payments, similar to a rental agreement, but with the added advantage of having the option to own the product outright eventually. This arrangement is particularly appealing for those who need immediate use of an item but may not have the funds for a full purchase upfront or are uncertain about committing to a direct purchase. It’s also beneficial for products that rapidly evolve or depreciate, like technology gadgets, where consumers might prefer to test or use the product before deciding on a full investment. For retailers, offering lease-to-own options can attract a wider range of customers, including those who are credit challenged, and can lead to increased sales, customer loyalty, and market reach. This purchasing method not only enhances accessibility to products but also provides consumers with the financial flexibility to manage their budgets effectively while enjoying the benefits of the leased items.

Installment loans

Installment loans offer a robust financing solution for consumers and businesses making big-ticket purchases, allowing them to spread the cost over an extended period. This type of loan is particularly suited for high-value one-time purchases such as fitness equipment, elective medical procedures and home improvement projects, where paying the full price upfront can be financially daunting. With long-term installment loans, the total cost is divided into smaller, manageable payments, typically made monthly. This approach not only makes expensive purchases more accessible but also helps in budgeting and financial planning, as repayments are predictable and spread out over time. The extended duration of these loans, which can range from 6 months to several years, reduces the monthly financial burden on the borrower, making it easier to manage alongside other financial commitments. For retailers, practitioners and contractors, offering long-term installment loans can broaden their customer base to include those who prefer or require a more extended repayment plan. It’s an effective strategy to increase sales of higher-priced items while also building customer trust and loyalty, as it demonstrates a commitment to providing flexible financial solutions. By accommodating the diverse financial situations of customers, installment loans play a pivotal role in making significant investments more attainable and financially sustainable.

Revolving line of credit

Revolving lines of credit (revolving credit) offer a dynamic and flexible financing option, particularly useful for consumers and businesses seeking repeat purchases. Unlike traditional loans with a fixed amount and a set repayment schedule, a revolving line of credit provides a predetermined credit limit that customers can draw from, repay, and reuse as needed. This flexibility is key: it allows users to borrow exactly what they need, when they need it, up to the limit of the credit line. Interest is typically charged only on the amount borrowed, not on the entire credit limit, making it a cost-effective option for managing fluctuating financial needs.

Retailers and service providers offering a revolving line of credit can enhance customer loyalty by providing a reliable, reusable financial resource. This not only improves the customer experience by offering financial flexibility but also encourages repeat transactions, as the ease of access to credit can facilitate ongoing purchasing decisions. By aligning with the financial needs and preferences of customers, revolving lines of credit represent a versatile and strategic approach to consumer and business financing.

Choosing the right POS financing option

When selecting the right type of POS financing for your customers, it’s crucial to consider their specific needs, purchasing behaviors, and the nature of your products or services. Start by analyzing your customer base: Are they typically making large, one-time purchases, or do they prefer smaller, recurring transactions? Understanding this dynamic helps in choosing between options like BNPL for immediate, smaller purchases or long-term installment loans for big ticket items. Additionally, consider the speed and convenience of the application process, as this can greatly influence customer satisfaction. For businesses, B2B financing might be more appropriate, while consumers might prefer the flexibility of lease-to-own options for certain goods. The key to a successful POS financing strategy lies in offering a range of options to cater to diverse customer needs.

Adopting a platform-first approach is highly effective in this context. By integrating a POS lending platform, you can embed multiple financing options into your point of sale. This not only provides customers with a variety of choices but also streamlines the financing process, making it more efficient and user-friendly. Such a system allows for a seamless combination of different financing methods, such as revolving credit lines for larger purchases and BNPL for smaller purchases, ensuring that each customer finds a solution that best fits their financial situation. Ultimately, a platform-first approach offers the flexibility and adaptability needed to meet the evolving demands of both your business and your customers, leading to enhanced customer satisfaction and potentially higher sales volumes.

Future of POS financing

The future of POS financing is to empower the consumer to make purchases at the point of decision, whenever and wherever that might occur.. The increasing shift towards omnichannel, digital, and mobile platforms, will likely lead to more integrated and user-friendly POS financing options within online and in-person and even combined shopping experiences. Additionally, there’s a potential for diversification in financing options, such as the incorporation of flexible payment plans tailored to individual consumer needs or the introduction of new financing models that could include more peer-to-peer elements or blockchain technology.

Another important trend is the growing consumer demand for transparency and simplicity in financing. This could lead to more straightforward, easy-to-understand financing options with clear terms and conditions, catering to a market that values financial clarity. Furthermore, the rising emphasis on financial inclusivity might drive the expansion of POS financing to cover a broader range of products and services, making it accessible to a wider segment of the population.

Finally, regulatory changes and an increased focus on consumer protection could shape the future of POS financing, potentially leading to more standardized practices across the industry. These changes will not only enhance the customer experience but also provide businesses with new opportunities to innovate in their sales and financing strategies, ensuring that POS financing remains a vital component in the evolving landscape of consumer purchasing.

Conclusion

In conclusion, POS financing has evolved to a multiple-lender model, employing the concept of waterfall financing within an embedded lending platform. This innovative approach will revolutionize the way businesses and consumers interact with financing options. By integrating a variety of lenders into a single, seamless platform, merchants can offer a more diverse range of financing solutions, ensuring that there’s a fit for every customer’s unique financial situation. The waterfall financing aspect further enhances this model, as it systematically routes customer applications through different lenders based on predefined criteria, thereby increasing approval rates and providing customers with the best possible financing terms. This embedded lending platform not only simplifies the financing process for customers but also for merchants who benefit from a single platform for all their POS financing management. Looking ahead, the adoption of a comprehensive, customer-centric approach in POS financing will be a key driver in the evolution of consumer purchasing experiences, marking a leap forward in the intersection of finance and retail.

Kevin has worked in the banking and finance industry for over a decade. He has worked closely with some of North America’s largest banks, financial institutions, and retailers. Kevin is an expert in embedded consumer financing and B2B financing and has a deep understanding of current trends and where the industry is heading.

Offering patients a seamless path to dental financing choices is a strategic must for dental providers in 2024. More patients than ever before are exploring financing options as demand for elective treatments rises. To meet this demand, dental providers must offer diverse financing solutions that cater to a broad spectrum of patient needs. With an embedded lending platform, you can easily provide your patients with seamless access to multiple lenders to offer the best dental financing for patients.

An embedding lending platform simplifies the financing process, enabling dental practices to offer multiple financing options. The platform integrates directly into a dental service’s existing systems, allowing patients to apply for dental financing options without leaving the dentist’s office, website, or call center. In doing so, dental providers can enhance customer loyalty by ensuring a favorable financing experience with approval rates of up to 85% for their patients.

Navigating dental financing: opportunities and pitfalls

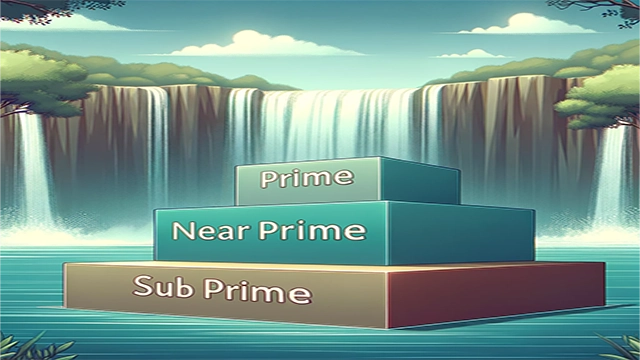

Lenders categorize borrowers based on their credit scores. ‘Prime’ are those with excellent credit, ‘near-prime’ those with good but not perfect credit, and ‘subprime’ those with poor credit histories. To meet the needs of patients across this spectrum of credit, dental providers must incorporate multiple lenders into their financing offerings. This is a process fraught with challenges if handled independently, as:

Lender integrations are complex, time-consuming, and require significant resources.

Day-to-day management of each lender is complex and time-consuming.

Dependency on single lenders becomes risky if terms change or if a financing provider ceases operations.

Patients may need to complete several applications before being approved, each with its own distinct set of requirements.

Staff must navigate and understand the systems of multiple lenders, each with its own processes.

The only way to counter such challenges is through a platform-first approach to point-of-sale financing. This will free dental practices up to focus on their core operations and patient care while providing an exceptional dental financing experience for their patients with higher approval rates and better conversion.

Enhance dental financing with platform-first approach

Streamlining access to personalized financing solutions is a game changer. By providing patients with a flexible and choice-driven financing experience, dental practices can dramatically enhance the patients’ purchasing experience and deliver high approval rates. As a result, dental practices observe a notable rise in the average transaction value, leading to an overall boost in sales, stronger patient relationships, and a competitive edge in the healthcare marketplace. An embedded lending platform:

Facilitates a seamless connection between dental practices, multiple lenders, and patients covering the entire credit spectrum on a single platform.

Simplifies the application process and enhances the patient’s experience wherever they are receiving service: in-clinic, through a call center, or online.

Results in high approval rates of up to 85% that in turn boost conversions.

Manages all financing activities efficiently, from a single application to instant approvals to post-sale management including disputes, reconciliations, and customized reporting.

Provides data and analytics to optimize the financing offer and create personalized relationships with patients.

Integrating an embedded lending platform into the patient care journey is the most effective way to meet these needs, providing a seamless financing experience for patients and clinics. Dental practices that integrate an embedded lending platform significantly improve the patient experience. Patients enjoy quicker service, with immediate access to a range of dental financing options tailored to their individual needs and financial situations, all without the need for multiple applications. This hassle-free approach to dental financing helps patients feel more at ease and valued, fostering a sense of loyalty and satisfaction with their dental care provider.

Why ChargeAfter is the platform of choice for dental practices

ChargeAfter’s embedded lending platform enables dental practices to seamlessly integrate financing into the patient journey, whether online, in clinics, or via call centers. The platform connects dental practices with a network of lenders that cater to a full range of patient credit profiles. Lenders on the platform offer a diverse range of financing products, including installment plans and revolving credit, to cater to various patient needs and preferences.

By simply filling out a quick application, patients are matched with the best financing options through a waterfall financing approach, where if a patient isn’t approved by the first lender due to their credit score, their application automatically ‘falls’ to the next lender in line until the best match is found. This process ensures that patients receive tailored dental financing solutions within seconds based on their individual credit needs and preferences. It is easy for dental practices to manage, supporting the entire financing process in a single platform enabling quick and easy refunds, reconciliations, dispute management, reporting, and lender optimization.

In 2024, personalizing patient financing will become not just an option but a necessity for dental practices aiming to distinguish themselves in a competitive landscape. As we navigate through a year of innovation and patient-centered care, offering tailored dental financing solutions will emerge as a key strategy to make patients smile wider than ever before.

Payments MAGnified 2024 by Merchant Advisory Groups (MAG) will take place from 20 Feb to 23 Feb 2024 at the Hyatt Regency Dallas. TX (USA)

If you are prioritizing enhancing your POS financing in 2024 and are heading to Payments MAGnified on February 21nd & 22nd – we would love to meet!

As the industry-leading embedded lending platform for point-of-sale financing, we can help you simplify the financing journey for you and your customers. Our easy-to-use platform and network of lenders deliver up to 85% approval rates making for happier customers and more sales.

Come and meet the team to learn how ChargeAfter can help you unlock the full potential of POS financing. You can find us at Booth 216 or schedule a meeting.

Payments MAGnified 2024 will delve deeper into the technology of payments, connecting merchant IT professionals and their business partners with technology sponsors through technology-focused educational sessions and engaging networking events. The MAG Tech Forum, aligned with the bi-annual MAG conference, is designed explicitly for payment IT professionals. It provides education and networking opportunities focused on innovative uses of new relevant payment technologies.

This event for professionals and businesses in the financial payments industry, offers networking opportunities and customizable experiences catered to business- and tech-minded individuals. Payments MAGnified is dedicated to exploring the depths of industry challenges and opportunities, focusing on new advances in payment technologies, consumer financing, and embedded financing, and other topics.

As shoppers increasingly lean towards flexible point-of-sale financing to pay for purchases and services, and merchants and other sellers seek the best way to meet this demand, the banking sector recognizes that it needs to expand its existing lending models and diversify POS financing offerings. This shift highlights that embedded lending is not just an emerging opportunity but a strategic necessity for banks to maintain their competitive edge.

The rise of embedded lending in point-of-sale finance

Consumer financing at the point of need is becoming an integral part of the customer journey, impacting the customer experience, business growth, and sales revenue. Continued economic challenges, such as the cost-of-living increase, alongside the emergence of on-demand loans at the point of sale to meet this need are changing how people pay for goods and services. In 2021, nearly 5% of U.S. financial transactions, totaling $2.6 trillion, were integrated into e-commerce and other software platforms, and this is set to reach over $7 trillion by 2026, according to Bain & Company.

Fintech companies have led the way in the point-of-sale (POS) financing revolution, especially with the emergence of Buy Now Pay Later (BNPL) loans. McKinsey & Company estimates that banks have experienced annual losses of $8 to $10 billion to fintech players, representing not only a financial setback but also a loss of a vital customer base – younger, tech-savvy consumers.

For banks, point-of-sale financing represents both a challenge and an opportunity. While this market has been dominated by fintechs, traditional banks and financial institutions are beginning to enter this market, and they do so with significant advantages.

Strategic advantage for banks in POS financing

Banks and traditional lending financial institutions enjoy advantages over newer fintech companies when it comes to point-of-sale financing. These advantages stem from their established infrastructure and years of experience as lenders, positioning them to become the leading provider of POS financing services for merchants and their customers. These four advantages distinguish banks from the newer fintech companies that have more recently entered the market.

Merchants seek reliable point-of-sale finance partners. Banks are known not only for their stability and balance sheets, but also their competitive rates, and secure data handling, making them ideal partners vs. a fintech that is reliant on external investors to float loans. It’s not only merchants that seek a trusted partner, but consumer trust in banks is stronger than ever, with many customers preferring bank loans over fintech options due to their established reputation and reliability. Pattamatta & Dabadghao (2022), highlight the significance of this trust, particularly for newer consumer financing options like point-of-sale financing where customers often gravitate towards the familiarity and dependability of big established banks. This is not just a matter of comfort; it reflects a deeper understanding that banks offer a level of security and regulatory compliance that newer fintech companies may not have achieved yet.

2. Regulatory compliance and expertise

The role of strict regulatory frameworks in shaping the banking sector cannot be overstated. Over the years, banks have not only adapted to these regulations but have also developed robust processes for compliance, and the banks are the leaders in regulatory and compliance regulations to protect their customers. This deep-rooted regulatory expertise provides banks with a critical edge, particularly in a financial landscape where new regulations, especially concerning fintech and innovative financing models like BNPL (Buy Now Pay Later), are rapidly evolving and are still unclear. Banks on the other hand are highly regulated and their core business is lending under strict regulatory guidance. Banks are better prepared for mass consumer finance growth.

The point-of-sale finance sector, which has grown significantly in popularity and scale, has inevitably drawn the attention of regulatory bodies, including the Consumer Financial Protection Bureau (CFPB). The CFPB’s move towards establishing industry-wide regulations is a response to the growing need for consumer protection in this sector. Banks, with their long history of adapting to regulatory changes and ensuring compliance, are uniquely positioned to navigate these new standards and in large are already compliant as lenders unlike fintech BNPL providers whose expertise in regulatory compliance is a significant advantage over their fintech counterparts, many of which are still in the early stages of grappling with complex financial regulations.

3. Risk management and credit expertise

Banks’ proficiency in risk management and credit assessment plays a pivotal role in their ability to effectively navigate the point-of-sale finance landscape. Their established frameworks for risk management are the result of years of experience and refinement and enable them to adeptly handle the unique credit risks associated with these financing models. Jakšič & Marinč (2018) underscore the importance of this expertise, noting that unlike many fintech companies that are relatively new to the scene, banks have a long history of assessing and managing credit risk. This expertise is not limited to evaluating the creditworthiness of borrowers; it extends to developing sophisticated models that can predict repayment behaviors, detect fraud, and anticipate market changes that could impact the risk profile of their lending portfolios.

4. Stronger financial backing

The recent economic climate, characterized by inflation and rising interest rates, presents a challenging landscape for lenders. In this environment, some POS finance providers, often limited by their financial resources, have found it increasingly difficult to sustain operations. They face the dual challenge of adapting to market pressures while also trying to maintain competitive rates and services. In some cases, these challenges have led to the adoption of complex and costly measures to stay afloat, impacting both their stability and the quality of services offered to customers.

Banks, in contrast, have a more robust foundation to draw upon. Their financial backing typically encompasses a diverse range of assets and substantial capital reserves. This allows them to absorb market shocks and economic downturns more effectively than their fintech counterparts. In practical terms, this stability means that banks can continue to offer competitive rates and reliable financial products even in times of economic stress.

Banks as pioneers in point-of-sale financing

In 2024, banks have a golden opportunity to emerge as leaders in the POS financing marketplace. By leveraging their established trust, regulatory expertise, risk management and credit expertise, and strong financial backing, they are well-positioned to offer innovative and reliable financing solutions to merchants and their customers.

Understanding and adapting to market changes allows banks not only to reclaim lost ground from fintechs but also to forge new paths in consumer financing. It is evident that embedded lending at the point of sale is not a fleeting trend – it’s a key aspect of the future of banking. With a comprehensive approach and strategic advantages, banks are poised to redefine the point-of-sale financing landscape, offering enhanced services that meet the evolving needs of consumers and merchants alike.

Jeffrey Tower EVP Global Business Development Jeff has over 20 years of experience driving revenue through building global brand awareness, business development, marketing, and sales departments focused on consumer financing, fintech, and eCommerce.

In 2024, sales channel strategies need to be diverse and optimized to suit the purchasing behaviors of the modern shopper. In this article, we explore sales channel strategies in more detail and share 3 benefits of a sales channel strategy that integrates waterfall consumer financing.

What is waterfall financing?

Waterfall financing, from a consumer financing perspective, is a method of consumer lending at the point of sale whereby a shopper loan or credit application passes through a series of lender tiers prioritized for receiving the best loan interest and terms to lower-tiered lenders offering the next best loan offer.

Here’s how it typically works:

First Tier Criteria: Initially, an application is evaluated against the strictest criteria. These criteria include a high credit score, low debt-to-income ratio, or other financial stability and creditworthiness indicators. Most applicants who meet these criteria are considered low-risk borrowers.

Subsequent Tiers: Applications not meeting the first tier’s stringent requirements are passed down to the next tier. Each successive tier has slightly more relaxed standards than the one before it. For instance, the second tier might accept lower credit scores or higher debt-to-income ratios.

Approval or Decline: This process continues until either the application is approved under one of the tiers’ criteria or fails to meet all tiers’ standards and is ultimately declined.

What is a sales channel strategy?

A sales channel strategy refers to the marketing tactics used across several sales channels. In the modern eCommerce landscape, a single sales channel is simply not enough. Online stores should utilize a variety of channels, from social media platforms to Google Shopping and beyond, to attract new customers and retain existing shoppers. A sales channel strategy considers how best to engage consumers through online marketplaces, modern marketplaces, wholesale selling, retail selling, and paid advertising. Using a combination of platforms within these avenues will lead to greater sales channel success.

Waterfall financing from ChargeAfter will also support your sales channel strategy by empowering your customers’ purchases. By partnering with ChargeAfter, you can offer your customers access to a wide network of lenders capable of facilitating their shopping needs across your entire sales channel strategy. Let’s take a closer look at the benefits of a sales channel strategy that integrates waterfall consumer financing.

Benefits of waterfall financing

Benefits for shoppers

Waterfall financing makes shopping more accessible than ever. Merchants that use waterfall financing give their shoppers access to lenders who can finance their shopping decisions. Customers can receive this financing without having to undergo credit checks, making consumer financing a feasible choice for shoppers unwilling to turn to their financial institution for support. This, coupled with favorable repayment plans makes for an efficient shopping experience that appeals to new and existing customers.

Increased access to credit: Waterfall financing allows individuals who might not meet the strictest lending criteria to access credit still. This benefits those with lower credit scores or less conventional credit histories.

Opportunities to build or repair credit: For borrowers looking to build or repair their credit, gaining access to credit through less stringent tiers can provide this opportunity as long as they manage their debt responsibly.

Tailored financial products: Since waterfall financing involves different tiers with varying criteria, consumers might find products more tailored to their financial situation rather than a one-size-fits-all approach.

Benefits for lenders

Market expansion: This approach allows lenders to serve a broader range of customers. They can cater to prime borrowers in the upper tiers while offering products to near-prime or subprime borrowers in lower tiers, thus expanding their market reach.

Improved loan performance: Using more detailed criteria to assess borrowers, lenders can better predict loan performance and reduce default rates. Each tier can be optimized based on the risk profile and past performance of borrowers in that category.

Flexibility and responsiveness: Waterfall financing provides a framework for lenders to quickly adjust their lending criteria in response to changing market conditions, regulatory environments, or shifts in their risk appetite.

Data-driven decisions: This approach often relies on comprehensive data analysis, allowing lenders to make more informed and precise decisions based on various variables beyond just credit scores.

Industry benefits:

Financial inclusion: By providing credit opportunities to those whom traditional criteria might exclude, waterfall financing contributes to financial inclusion efforts.

Innovation in lending: This approach encourages innovation in the lending industry as lenders develop more sophisticated models to assess borrower risk across different tiers.

In summary, waterfall financing offers a more nuanced and flexible approach to lending that can benefit a wide range of consumers, especially those who might be underserved by traditional models, while also allowing lenders to manage risk and expand their customer base.

Originally published: 12 Jan 2022 Updated: 24 Jan 2024