6 POS Financing Solutions for Your Point of Sale

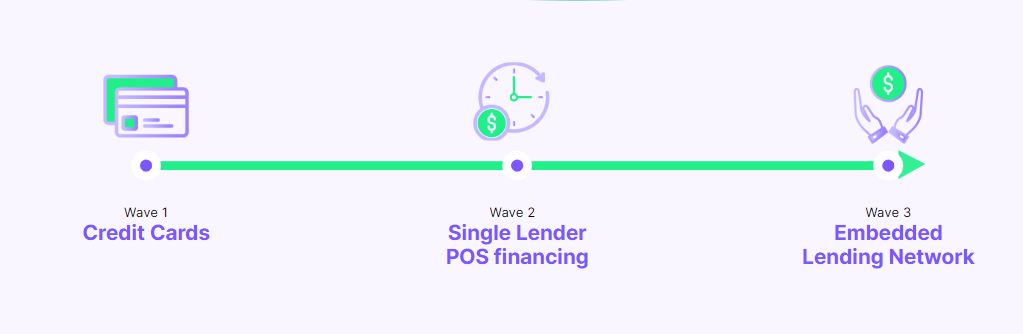

Point-of-sale (POS) financing encompasses six primary lending products: 0% APR financing, installment loans, revolving credit, consumer BNPL, business BNPL, and lease-to-own that allow customers to pay for purchases over time. By moving beyond single-lender models to multi-lender orchestration, merchants can connect customers with the right credit product at the moment of need, increasing approval rates and conversion while optimizing customer lifetime value.

What you’ll learn

- What POS financing means and why it’s growing

- The 6 main types of POS financing, and how each works

- Which options fit small purchases vs. big-ticket items

- How to choose the right mix for your business

- Where POS financing is headed next

What is POS financing?

With the right partner, financing becomes a growth engine.

Point-of-sale (POS) financing is a rapidly growing industry. According to McKinsey, POS financing balances have consistently expanded at a clip of 18% to 20% annually. In 2025, the Federal Reserve tracked six of the largest Buy Now, Pay Later (BNPL) providers and found they originated nearly $160 billion in consumer credit. Crucially, the Fed’s data focused only on these specific fintech providers while entirely excluding other segments of the POS financing market, such as revolving credit and lease-to-own, as well as other similar providers.

Growth has been driven by the expansion of fintech lenders, increasing demand for flexible payment options, and merchants embedding financing directly into the purchasing journey.

What are the 6 main types of POS financing?

The six main types of point-of-sale (POS) financing are 0% APR financing, installment loans, revolving credit, consumer BNPL, business BNPL, and lease-to-own (LTO). While they all enable customers to pay over time, they differ in eligibility, repayment structure, and the types of purchases they support.

6 POS financing solutions at a glance

| Type | Best for | Customer Profile | Typical Term | Cost Structure |

|---|---|---|---|---|

| 0% APR Financing | Big-ticket purchases | Prime | 6 to 24 months | 0% APR |

| Installment Loans | Major one-time purchases | Prime, Near Prime, Subprime | Typically 6–24 months (can extend to 60 months) | Fixed APR (usually 5%–36%), linked to the shopper’s credit score |

| Revolving Credit | Repeat purchases | Prime, Near Prime | Ongoing / Open-ended | Variable APR (usually 15%–30%+ on unpaid balances) |

| Consumer BNPL | Everyday and mid-size purchases | Prime, Near Prime | 4 payments over 6–8 weeks | 0% APR; late fees usually between $8–$10 |

| Business BNPL (B2B) | B2B corporate transactions & SMBs | Businesses | 30 days to 12 months (Net terms) | 0% interest for net terms; extension fees |

| Lease-to-Own | Durable consumer goods (e.g. furniture, appliances, auto accessories) | No-credit-required | 12–24 months | No APR, but high lease fees. Example: On a $1,000 item, pay $1,075 if paid in 90 days, or $2,100 over 12 months. |

1. 0% APR financing for big-ticket purchases

0% APR financing allows qualified customers to spread the cost of a purchase over monthly payments without paying interest during a promotional period. Typically structured as an installment loan, it is commonly used for higher-value purchases such as furniture, appliances, and consumer electronics, making large purchases accessible without requiring customers to pay interest.

For merchants, 0% APR financing can increase conversion rates and average order value without discounting products. By reducing the cost of financing rather than the price of the item, retailers can attract creditworthy customers while protecting margins.

2. Installment loans for major purchases

Installment loans allow customers to spread the cost of a purchase into fixed monthly payments over a predetermined period, typically from six months to several years. Many installment loans charge interest, although some are offered with promotional 0% APR depending on the lender and financing program.

For merchants, installment loans expand financing availability across a broader range of credit profiles, helping more customers afford larger purchases. Their longer repayment terms reduce monthly payments, making them well suited to higher-value purchases such as home improvement projects, elective healthcare, furniture, and fitness equipment.

3. Revolving credit for repeat purchases

Revolving credit gives customers access to a reusable line of credit that they can borrow from, repay, and use again over time. Unlike installment loans, there is no fixed repayment schedule for the entire credit line, and customers only pay interest on the outstanding balance. Private label credit cards (PLCCs) are one of the most common forms of revolving credit offered at the point of sale. 0% deferred interest financing may be offered for 6 – 24 months depending on the lender.

For merchants, revolving credit encourages repeat purchases by giving customers ongoing access to financing without requiring a new application for every transaction. It is particularly effective for retailers with loyal, returning customers, helping increase customer lifetime value while supporting larger and more frequent purchases.

4.Consumer BNPL for everyday purchases

Consumer Buy Now, Pay Later (BNPL) enables shoppers to split purchases into a series of manageable payments, interest-free for pay-in-4 installments. Available directly at checkout, BNPL is designed for speed and convenience, offering a streamlined application process and instant lending decisions that help customers complete their purchases.

For merchants, consumer BNPL can increase conversion rates, reduce cart abandonment, and attract customers looking for flexible payment options without committing to a traditional credit card. While commonly associated with smaller everyday purchases, many BNPL providers now also support higher-value transactions through longer-term installment plans.

5. Business BNPL for B2B transactions

Business Buy Now, Pay Later (BNPL), also known as B2B financing, enables businesses to purchase goods or services immediately while paying over time. Repayment terms typically range from 30 days to 12 months or longer, helping businesses preserve working capital and better manage cash flow.

For merchants and suppliers, business financing removes a significant barrier to purchase by giving commercial buyers greater payment flexibility. It can increase sales, encourage larger orders, and strengthen customer relationships by making it easier for businesses to invest in equipment, inventory, and other high-value purchases without paying the full amount upfront.

6. Lease-to-own for credit-challenged customers

Lease-to-own (LTO) enables customers to lease a product with the option to purchase it over time through regular payments. Unlike traditional financing, LTO typically does not require a strong credit history, making it accessible to customers who may not qualify for other financing options.

For merchants, lease-to-own expands financing availability to a broader range of customers, helping recover sales that might otherwise be lost. It is commonly offered for products such as furniture, appliances, electronics, and mattresses, allowing retailers to increase approvals while serving customers across the credit spectrum.

How can merchants offer the right POS financing mix?

There is no single financing solution that works for every customer or every purchase. The goal isn’t to choose the best financing product. It’s to match each customer with the financing option that’s best for them.

The most effective POS financing programs are created for different credit profiles, purchase sizes, and shopping journeys. When designing a financing strategy, merchants should consider:

- Average order value. Higher-value purchases often benefit from installment loans or 0% APR financing, while lower-ticket purchases may perform better with consumer BNPL.

- Customer profile. A mix of financing options helps serve prime, near-prime, and credit-challenged customers.

- Sales channel. Financing should work consistently across online, in-store, in-home, and call center experiences.

- Business model. Merchants selling to both consumers and businesses may need both consumer and B2B financing options, ideally within the same platform.

- Program flexibility. An independent financing platform makes it easier to add or replace lenders, expand financing products, and optimize performance over time without disrupting the customer experience.

Rather than relying on a single lender or financing product, many enterprise merchants use a platform to offer multiple financing options through a single integration. This approach increases approval rates, improves customer choice, and gives merchants the flexibility to adapt their financing program as customer needs and lender strategies evolve.

What’s the future of POS financing?

Point-of-sale financing is entering the era of agentic commerce. As AI agents become capable of researching products, comparing prices, and initiating purchases on behalf of consumers, they’ll increasingly participate in financing decisions as well. Rather than customers manually evaluating financing options at checkout, AI agents are likely to identify and recommend the most appropriate financing solution before the purchase is completed.

For merchants, this makes financing flexibility more important than ever. AI agents will only be able to recommend the best financing option if multiple products and lenders are available to choose from. Platforms that orchestrate a broad network of financing providers will be better positioned for an AI-driven commerce ecosystem than those tied to a single lender or financing product.

How ChargeAfter powers multi-lender POS financing

ChargeAfter enables merchants to offer multiple financing products through a single embedded lending platform. Its waterfall technology automatically routes each application across participating lenders based on the merchant’s configured financing strategy, helping maximize approvals without requiring customers to complete multiple applications.

Rather than integrating individual financing providers one by one, merchants connect once and gain the flexibility to offer a broad mix of financing products through a consistent checkout experience. As financing programs evolve, lenders and financing options can be added or replaced without disrupting the customer journey.

What does ChargeAfter’s platform offer?

No single financing solution meets the needs of every customer. ChargeAfter enables merchants to offer a full spectrum of financing products through a single platform, eliminating the need to manage multiple lender integrations while delivering a consistent financing experience across online, in-store, in-home, and call center channels. Key capabilities include:

- A single integration supporting 0% APR financing, consumer BNPL, business BNPL, lease-to-own, installment loans, and revolving credit

- A network of prime, near-prime, and subprime lenders accessed through a single application

Intelligent application routing with waterfall financing to maximize approvals - Omnichannel financing across online, in-store, in-home, and call center experiences

- Centralized reporting and program management across lenders and financing products

- White-label checkout that keeps the financing experience consistent with your brand

- The flexibility to add or replace lenders without changing your checkout experience

Key takeaways

- Point-of-sale financing includes six primary financing types: 0% APR financing, consumer BNPL, business BNPL, lease-to-own, installment loans, and revolving credit.

- Each financing type serves different purchase sizes, customer needs, and credit profiles.

- Merchants achieve the best results by offering multiple financing options rather than relying on a single lender or financing product.

- Multi-lender orchestration and waterfall financing help increase approvals by automatically matching customers with eligible financing providers.

- A single embedded lending platform simplifies program management while giving merchants the flexibility to evolve their financing strategy over time.

Frequently Asked Questions

Buy Now, Pay Later (BNPL) typically enables customers to split purchases into a small number of payments, often with interest-free options for shorter repayment terms. Installment loans generally support larger purchases with fixed monthly payments over longer periods, ranging from several months to several years. While both allow customers to pay over time, installment loans are typically used for higher-value purchases and may include interest depending on the financing program.

Both 0% APR financing and BNPL allow customers to spread the cost of a purchase over time, but they serve different purposes. 0% APR financing is a promotional offer that enables qualified customers to finance larger purchases without paying interest during a set promotional period. BNPL is designed for fast, embedded checkout experiences and may offer both shorter-term interest-free payments and longer-term installment financing, depending on the provider.

Offering multiple POS financing options increases approval rates by giving more customers access to financing that matches their credit profile and the size of their purchase. Instead of relying on a single lender or financing product, multi-lender platforms can match each application with the most appropriate financing option, helping reduce declines and recover sales that might otherwise be lost.

Yes. B2B financing is designed for business purchases and often includes repayment terms ranging from 30 days to 12 months or longer. Underwriting is based on business information rather than consumer credit, and financing is commonly used for purchasing inventory or equipment. Consumer POS financing, by contrast, is designed for individual shoppers purchasing goods or services for personal use.

The right financing mix depends on factors such as average order value, customer demographics, and the products being sold. Many merchants offer multiple financing options to serve different purchase sizes and credit profiles. Embedded lending platforms make it possible to manage those options through a single integration.

Waterfall financing automatically routes a single customer application through multiple participating lenders based on predefined rules. Applications are typically presented to the lenders offering the best financing options for that customer’s credit profile first. If declined, the application is automatically routed to the next eligible lender, helping merchants maximize approvals while giving customers access to the most appropriate financing available.