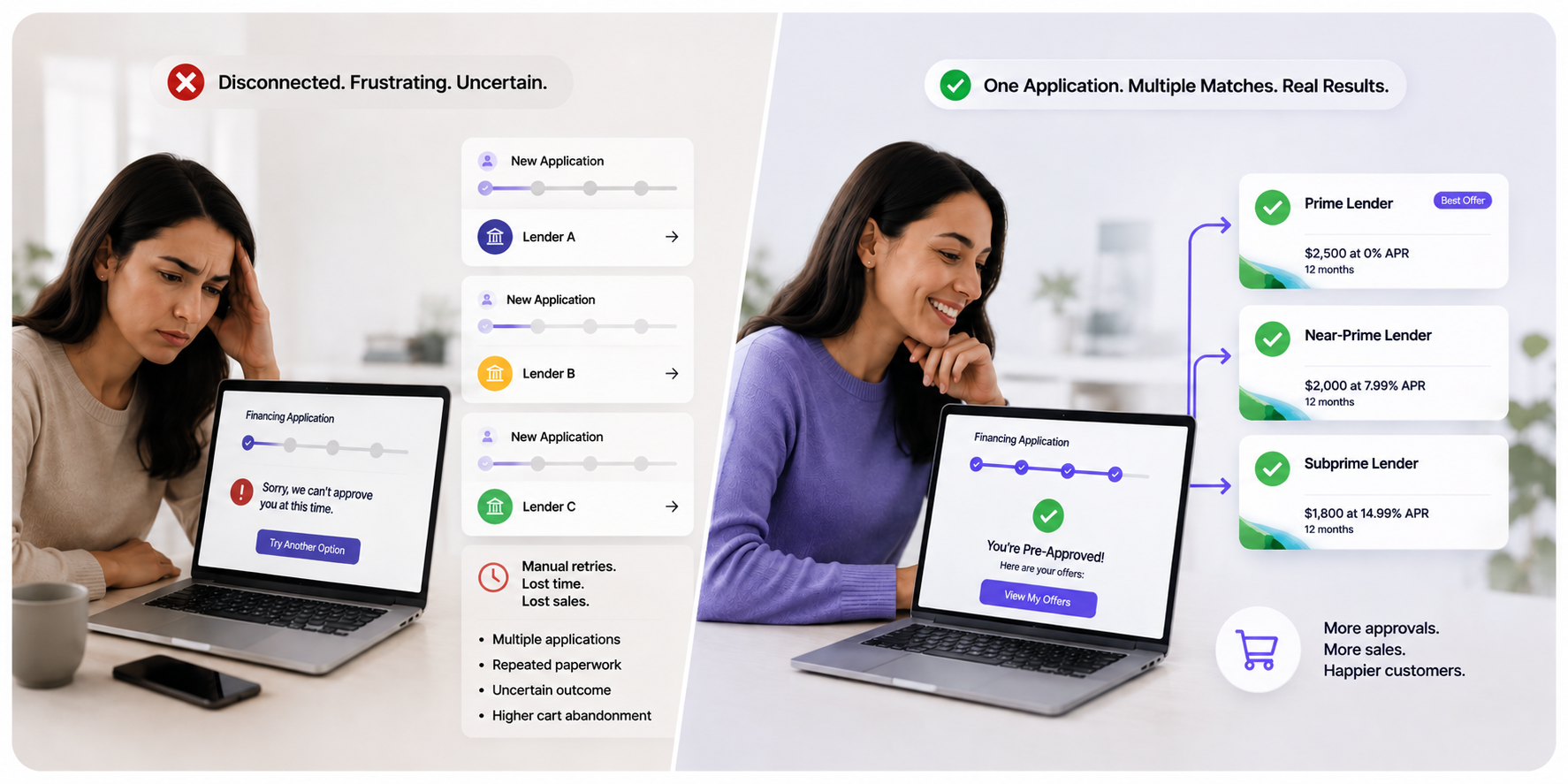

Lender orchestration is transforming point-of-sale financing. Rather than depend on a collection of individual financing programs, orchestration enables merchants to implement intelligent, real-time multi-lender financing flows designed to maximize approvals, improve customer experience, and create greater checkout resiliency.

Category: Category name

Heading to Payments MAGnified? Let’s Talk Embedded Lending!

ChargeAfter Celebrates Multiple Wins in Furniture Today’s Reader Rankings, 2025

Find the Right Finance Partner for Your Home Improvement Business

Why Independence Matters in Embedded Lending: Choice, Control, and Trust for Merchants

We explore why independence matters in embedded lending, and how lender-neutral orchestration outperforms single-lender or captive platforms.

ChargeAfter Nominated for 4 Furniture Today Awards

Why Multi-Lender Platforms Are the Future of Home Improvement Financing

Explore financing options for home improvement contractors. Find the best solution for boosting revenue and streamlining operations.

Let’s Connect at MAG Payments Conference 2025, Booth 310

If you’re attending the conference and want to reform your point-of-sale financing, stop by booth 310 to discuss how our embedded lending platform can help you streamline your POS financing and boost approvals.