In today’s fast-paced digital landscape, the financial services industry is facing a pivotal moment. The rise of embedded finance is transforming how consumers interact with lending products, offering convenience, flexibility, and a more personalized financial experience. For banks and financial institutions (FIs) looking to capitalize on this trend, the key lies in adopting scalable, secure, and flexible solutions that can be integrated seamlessly into their existing infrastructure. ChargeAfter’s Lending Hub represents a significant leap forward in this domain, empowering banks to provide customized, embedded finance solutions at various points of sale.

As leaders in technology, product development, and business strategy, it’s essential to understand how ChargeAfter’s Lending Hub is not only a powerful tool for banks but also a transformative technology for the future of lending. This article explores how the platform addresses the challenges of modern financial services and how it empowers institutions to stay competitive.

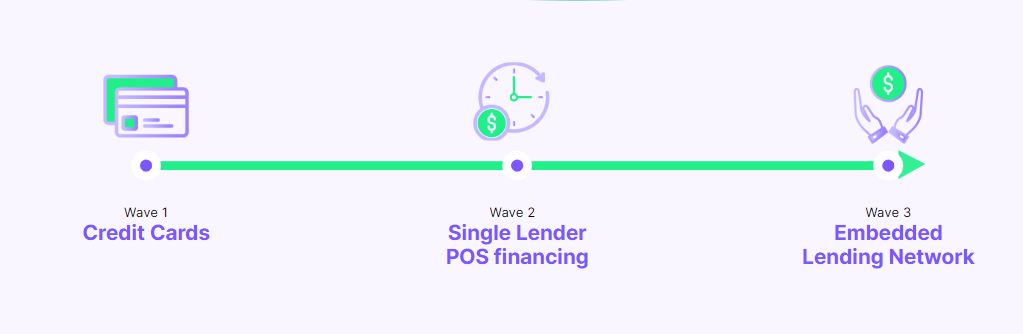

The rise of embedded finance in banking

The traditional boundaries of banking are dissolving. Consumers no longer see lending as a separate, siloed function but as an integrated part of their purchasing journey. Whether shopping online, in-store, or on mobile apps, consumers expect financial services to be readily available at their fingertips. Embedded finance allows this by integrating lending products directly into the purchase experience, providing an instant, frictionless way for customers to access credit when they need it most.

For banks, this shift presents both an opportunity and a challenge. On one hand, embedded finance opens new revenue streams and deepens customer relationships. On the other, it requires the right technological infrastructure to deploy these products in a scalable and compliant manner.

This is where ChargeAfter’s Lending Hub comes into play.

What is ChargeAfter’s lending hub?

ChargeAfter’s Lending Hub is a cloud-based, white-label platform that enables banks to offer a full suite of lending products—including revolving credit, installment loans, Buy Now, Pay Later (BNPL), and personal loans—directly at the point of sale. The platform is designed with flexibility and scalability in mind, providing banks with the tools to create, distribute, and manage customized financial products through various channels such as eCommerce, in-store, and mobile applications.

Unlike traditional lending systems that require significant infrastructure investments, ChargeAfter’s platform operates as a plug-and-play solution, allowing banks to get up and running with embedded lending products quickly and efficiently. The system’s microservices architecture ensures that it can scale to meet the needs of even the largest institutions while maintaining a high degree of flexibility.

Key features that set the lending hub apart

- White-Label Solution: ChargeAfter’s Lending Hub offers a fully white-labeled experience, enabling banks to maintain complete control over their branding and merchant relationships. This allows banks to present themselves as the primary financial partner while leveraging ChargeAfter’s robust technology stack behind the scenes.

- Lender Matching Engine: The patented lender matching engine is a critical feature that sets ChargeAfter apart. This engine helps banks match consumers with the most appropriate lending products based on their credit profiles, increasing approval rates and ensuring consumers have access to the best possible terms. For banks, this means higher conversion rates and the ability to serve a broader range of customers.

- Omnichannel Capabilities: One of the biggest challenges banks face today is creating a seamless experience across multiple touchpoints. ChargeAfter’s Lending Hub integrates with eCommerce platforms, POS systems, self-checkout kiosks, and mobile applications, ensuring that customers can access credit anytime, anywhere. Whether a consumer is shopping online, in-store, or through a mobile app, they are presented with tailored financing options at the point of need.

- Pre-Built Integrations: ChargeAfter’s platform comes with pre-built APIs, SDKs, and branded extensions that make it easy for banks to integrate lending products into their existing infrastructure. This plug-and-play capability significantly reduces time-to-market, enabling banks to deploy embedded finance solutions faster than ever before.

- Advanced Analytics: The platform offers a robust suite of analytics tools that allow banks to track performance across their lending programs. From real-time KPIs to deep insights into consumer behavior, ChargeAfter’s analytics capabilities help banks optimize their lending strategies and improve operational efficiency.

- Compliance and Security: As regulations around data privacy and financial services tighten globally, compliance is more critical than ever. ChargeAfter’s Lending Hub is fully compliant with PCI DSS, ISO 27001, and GDPR standards, providing banks with peace of mind that their data and their customers’ data are handled with the utmost security.

Why banks should embrace embedded finance

For banks and lending FIs, embracing embedded finance is no longer a question of “if” but “when.” By integrating lending products directly into the consumer purchase journey, banks can drive higher engagement, boost loan origination, and create more meaningful relationships with their customers.

Furthermore, embedded finance opens up new opportunities for growth. With the right technology in place, banks can expand their reach beyond traditional banking environments, partnering with merchants across various industries to provide tailored lending solutions.

ChargeAfter’s Lending Hub offers the ideal platform for banks looking to stay ahead of the curve. Its combination of scalability, flexibility, and speed-to-market makes it a powerful enabler of embedded finance strategies, allowing banks to not only meet the needs of today’s consumers but also to anticipate the demands of tomorrow’s market.

Conclusion

As embedded finance continues to reshape the financial services landscape, ChargeAfter’s Lending Hub provides a best-in-class solution for banks and financial institutions looking to offer innovative lending products at the point of sale. By leveraging this powerful platform, banks can enhance their customer experience, improve operational efficiency, and drive sustainable growth.

The future of lending is embedded. And with ChargeAfter’s Lending Hub, that future is within reach.

About Jeffrey Tower

EVP Global Business Development and Strategy

Jeff has over 20 years of experience driving revenue through building global brand awareness, business development, marketing, and sales departments focused on consumer financing, fintech, and eCommerce.