What is an embedded lending platform?

Embedded lending is a revolutionary approach to consumer financing. Embedded lending platform integrates directly into the merchant sales process, offering consumer financing options when they need them the most – during their purchase decision.

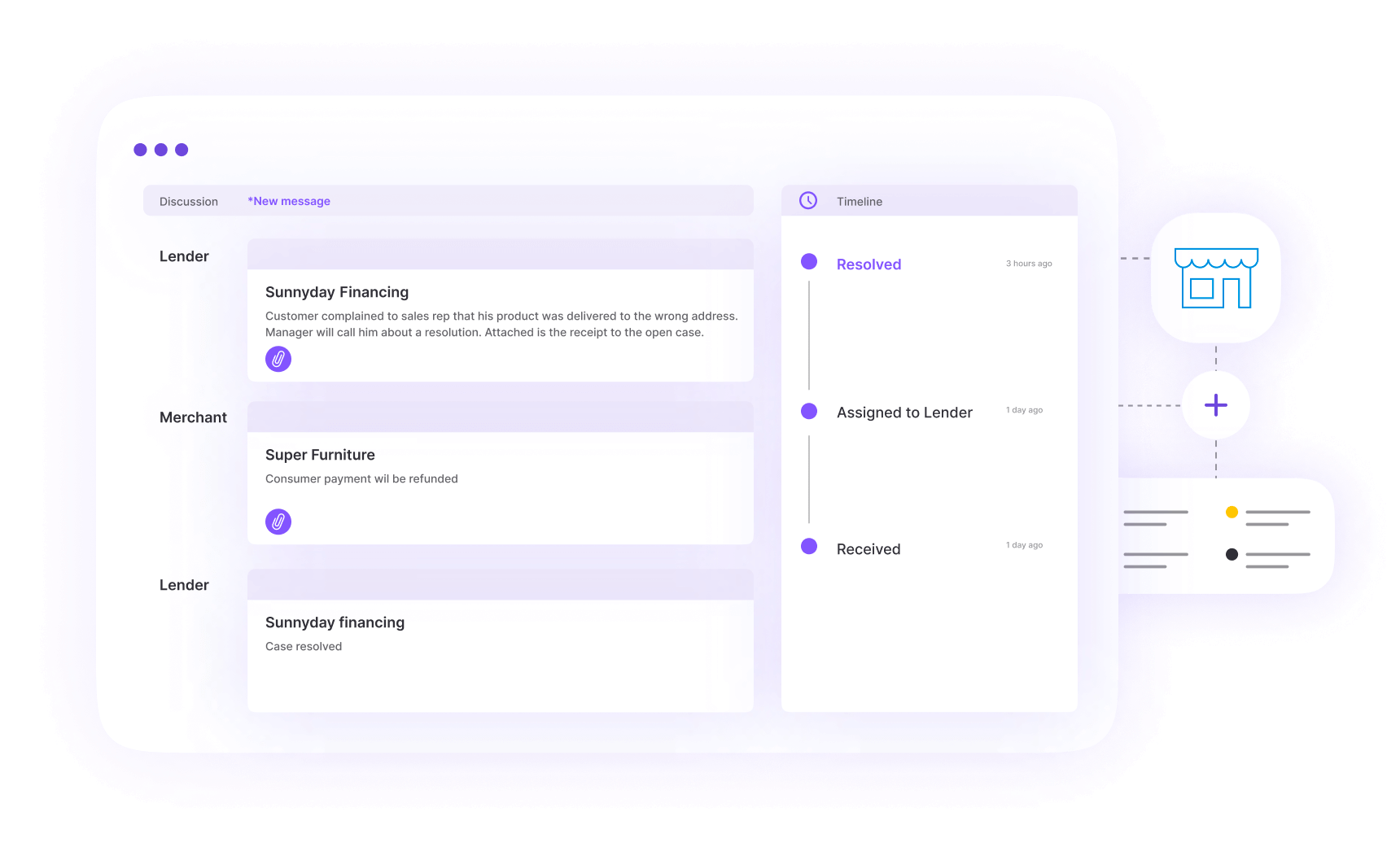

This seamless integration means customers can explore and choose financing solutions without leaving the merchants store or website. Embedded lending platforms are integrated with lenders to seamlessly bridge merchants’ customers at the point-of-sale directly to lenders allowing for an enhanced customer journey and omnichannel lending experience.

Benefits of embedded lending platform?

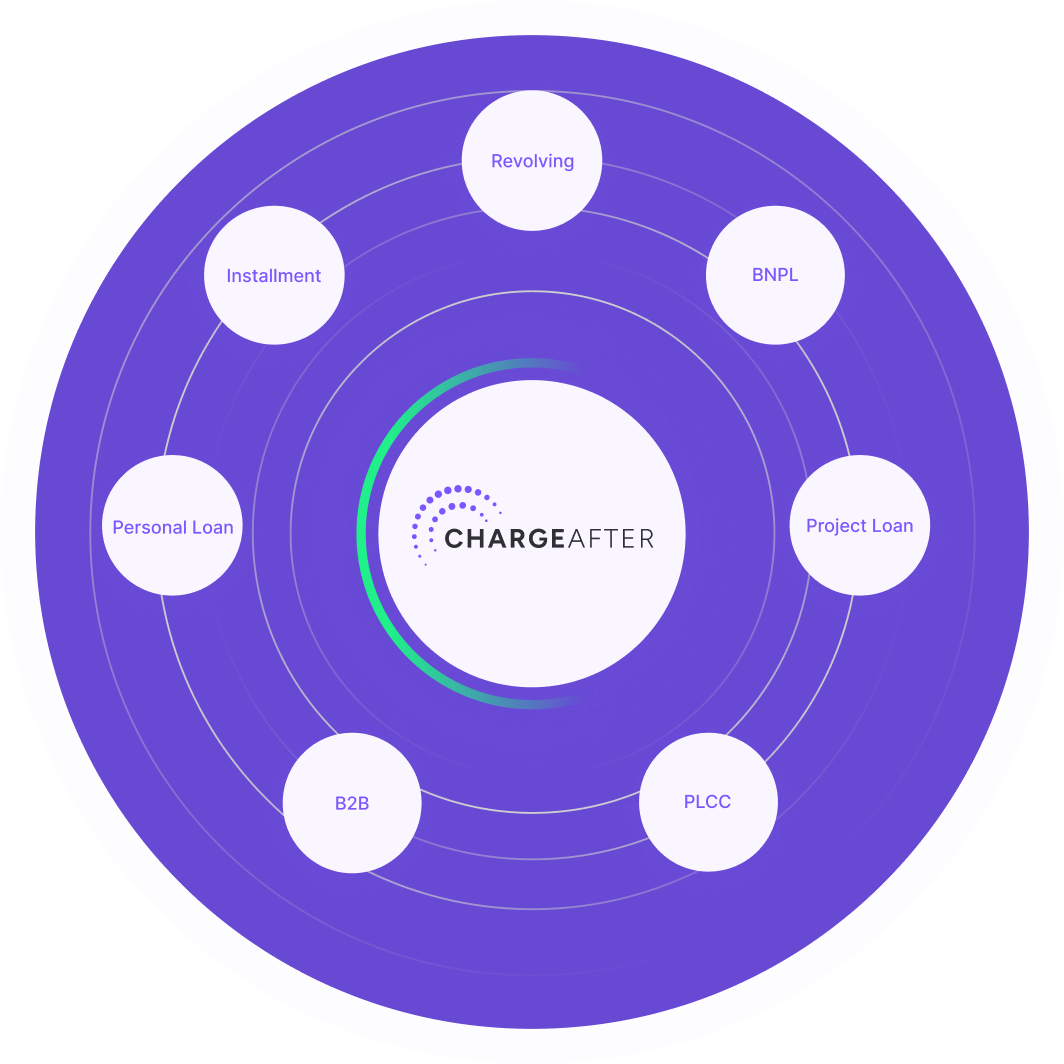

- Multi-Lender Accessibility: Some embedded lending platforms have multi-lender gateways, allowing you to connect with various financing providers. This ensures that customers can find consumer financing options that suit their needs and credit profile.

- Waterfall Financing Technology: Multi-lender gateways utilize the waterfall financing approach. These embedded lending platforms intelligently route customer applications to lenders most likely to approve them. This maximizes consumer financing approval rates and minimizes the time spent searching for suitable financing.

- Personalized Consumer Financing Choices: Power of choice; embedded lending platforms tailor consumer financing options to each customer’s unique profile, ensuring they receive relevant and attractive offers.

- Enhanced Customer Experience: By offering instant, personalized consumer financing options often incorporate omnichannel lending solutions to enhance the customer experience, increasing satisfaction and loyalty.

- Higher Conversion Rates: Embedding financing solutions into the purchase process significantly boosts conversion rates, as customers are more likely to complete a purchase when consumer financing is readily available.

- Streamlined Process: Embedded lending platforms simplify the consumer financing process for you and your customers, removing barriers and making transactions smoother and faster.

ChargeAfters’ embedded lending platform

ChargeAfter is more than just a consumer financing platform; it’s a tool to unlock potential sales and build lasting customer relationships. Whether in-store, online, or anywhere customers shop, ChargeAfter’s embedded lending platform ensures that customers across the credit spectrum can finance their purchases in a way that suits them.