Heading to Payments MAGnified? Let’s connect at booth 314! Book a meeting now February 10–13, 2025, Gaylord National Resort in National Harbor, MD.

Is point-of-sale financing a strategic priority in 2025? If so, you’re in good company—78% of merchants highlighted it as a key focus in our latest survey. Our team will be on hand at Payments MAGnified to discuss how we can help you streamline the omnichannel journey, boosting approvals, and delivering an outstanding customer experience.

Discover why our embedded lending platform is the platform of choice for leading merchants. Your customers benefit from greater personalization and choice, while your team enjoys a simple integration and end-to-end control of the lending journey on a single platform.

Money 2020 will take place from 27 Oct to 30 Oct 2024 in Las Vegas.

Are you heading out to Money 20/20? Our team will be on-site and ready to chat about how our Lending Hub helps banks revolutionize their embedded lending solutions through our scalable, secure, and flexible platform.

We invite you to reach out and connect with our team ahead of time! Meidad Sharon, Founder & CEO

Jeffrey Tower, EVP Global Business Development & Strategy

Nufar Bareket, Global Head of Partnerships and Financial Institutions

Jim Magnuson, Director of Sales And Business Development

Money20/20 USA remains the world’s most significant and influential event for the global financial ecosystem, encompassing sectors like banking, payments, technology, startups, retail, fintech, financial services, policy, and more. We are excited to connect with industry leaders and build scalable long-term partnerships.

As the holiday season approaches, retailers are gearing up to make the most of Black Friday and Cyber Monday in 2024. These shopping events have become critical for driving sales, and your strategies can make all the difference in your success. In this article, we share essential insights and actionable tips to help you optimize your approach.

Optimizing mobile experiences

With a significant portion of holiday shopping conducted on mobile devices, it’s essential that your website is mobile-friendly. Fast loading times, easy navigation, and a straightforward checkout process are crucial.

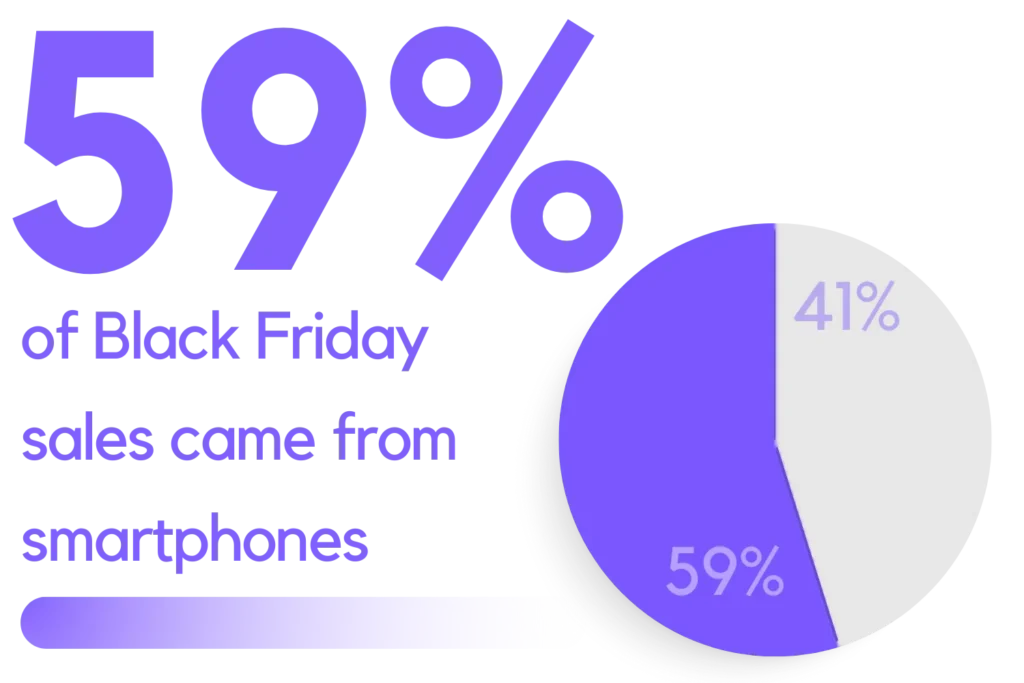

According to MobiLaud, 59% of Black Friday sales came from smartphones, a 55% increase from the previous year. Ensuring a seamless mobile experience can significantly reduce bounce rates and increase conversions, contributing to higher sales.

Leveraging social media for targeted ads

Investing in targeted social media advertising can drive traffic and conversions. Personalized ads resonate more with potential buyers, capturing their interest and encouraging them to visit your site. Platforms like Facebook, Instagram, and TikTok offer powerful tools for targeted campaigns, allowing you to reach a broader audience and engage with them meaningfully.

Effective social media strategies enhance brand visibility and attract more shoppers during the holiday season.

Ensuring seamless checkout processes

A smooth and quick checkout process can reduce cart abandonment, making the difference between a lost sale and a loyal customer. Streamlining the checkout process involves minimizing the steps required to complete a purchase, offering multiple payment options, and ensuring that the process is secure and user-friendly.

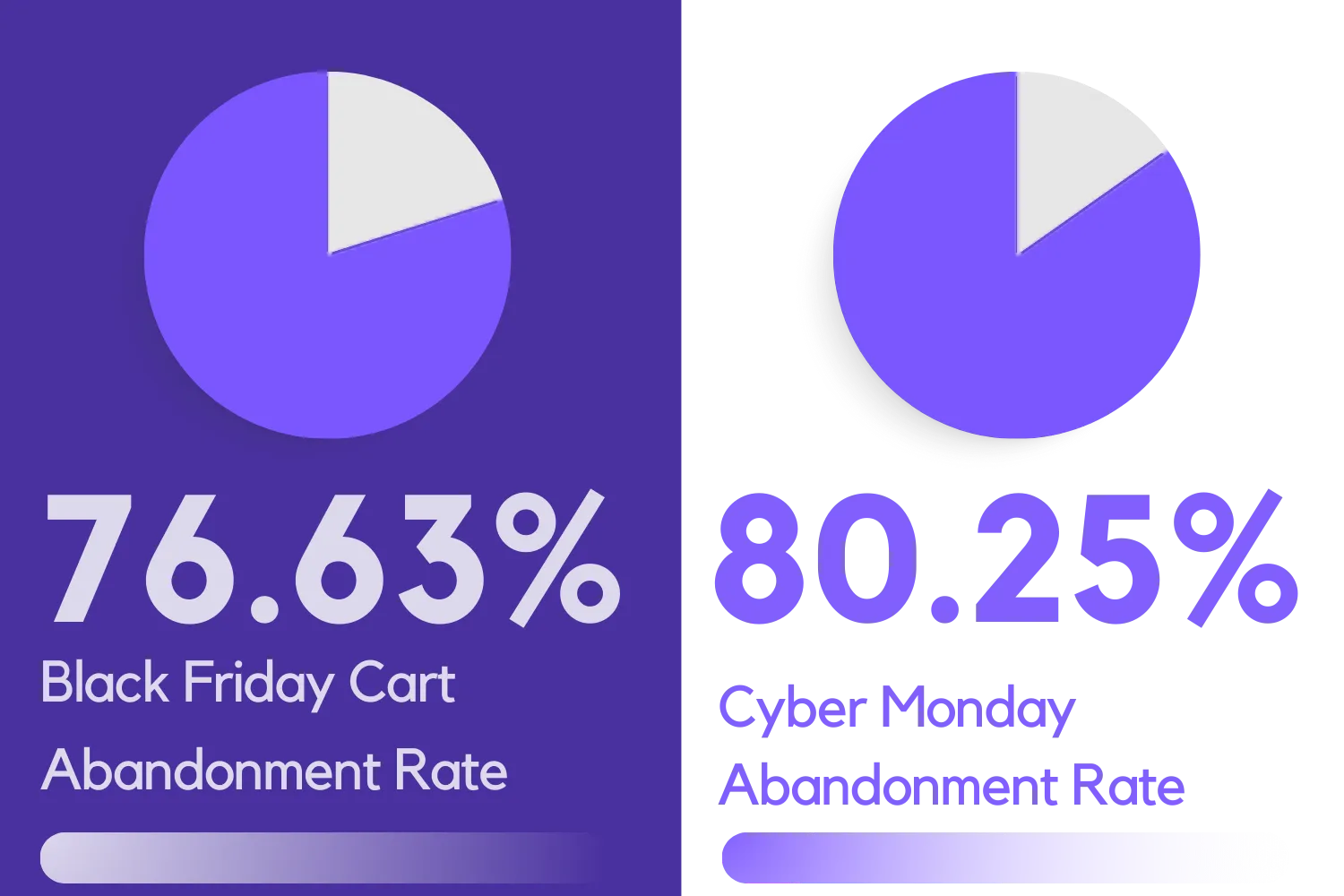

According to SaleCycle, the cart abandonment rate for Black Friday was 76.63%, and for Cyber Monday, it reached 80.25%. A seamless checkout experience can significantly enhance customer satisfaction and encourage repeat purchases.

Offering flexible financing options

Providing multiple financing options can significantly impact customer satisfaction and conversion rates. Shoppers who used a Buy Now, Pay Later (BNPL) service spent $598 on average on Black Friday, compared to $452 among those who didn’t use a deferred payment method (PYMNTS Intelligence).

By integrating platforms like ChargeAfter, retailers can offer a variety of financing options, catering to individual customer needs and enhancing the overall shopping experience. This flexibility is crucial during the high-traffic holiday season when shoppers are looking for the best deals and convenient payment methods.

Starting early: the early bird strategy

For the past several years, consumers have shown eagerness to sign up for brand email and text lists around Halloween. They know the holiday season is approaching and don’t want to miss out on sales or inventory announcements. While capturing opt-ins should be a year-round effort, Halloween is an ideal time to ramp up these efforts.

Retail trends show that holiday sales start earlier each year, meaning all product messaging, campaigns, email triggers, and identity strategies should be tested and ready to run by Halloween.

Website Pop-Ups: Use pop-ups with special offers or sign-up incentives after visitors have been on your site for a certain duration or just as they’re about to leave.

Influencers: Collaborate with influencers to create unique content that resonates with their audience. Partner for product giveaways or contests to boost visibility and engagement.

Social Media: Develop engaging content with polls, quizzes, and user-generated content. Create stories and reels on platforms like Instagram and TikTok for limited-time offers or behind-the-scenes looks.

Paid Ads: Launch retargeting ad campaigns to show ads to users who visited your site but didn’t make a purchase. Use platforms like Facebook to target lookalike audiences, reaching users similar to your existing customers.

Act now to unlock Black Friday / Cyber Monday success

To truly capitalize on Black Friday and Cyber Monday in 2024, start preparing now. Focus on optimizing mobile experiences, leveraging social media for targeted ads, ensuring seamless checkout processes, and offering flexible financing options like those provided by ChargeAfter. Boost sales, reduce cart abandonment, and create a memorable shopping experience that keeps customers coming back—retailers who use ChargeAfter see up to 85% POS financing approval rates.

Integrating the ChargeAfter platform is seamless and easy, with plenty of time to get set up before the holiday rush. Plus, our merchant portal is packed with powerful data and insights to help you manage lenders effortlessly and supercharge your post-season strategies.

Want to see how ChargeAfter can transform your holiday season sales?Schedule a demo with ChargeAfter today and unlock the potential of personalized financing!

Are you among the 78% of merchants prioritizing POS financing in the next 12-18 months*? If so, let’s connect! Our team is heading to MAG Payments and is available to discuss your POS financing challenges and see how our multi-lender waterfall platform can help you maximize your point-of-sale financing potential. Visit us at booth 214 or schedule a meeting with us. Swing by and you have a chance of winning a cool prize!

Panel Discussion

We are excited to invite you to attend our panel discussion Check your Balances: How Financial Inclusion is Defining a Generation with some of the biggest names in the industry.

Meidad Sharon – CEO & Founder, ChargeAfter

Jai Holtz – Vice President, Financial Services, Best Buy

Jay Waters, Senior Director Financial Services, Lowe’s Company Inc.

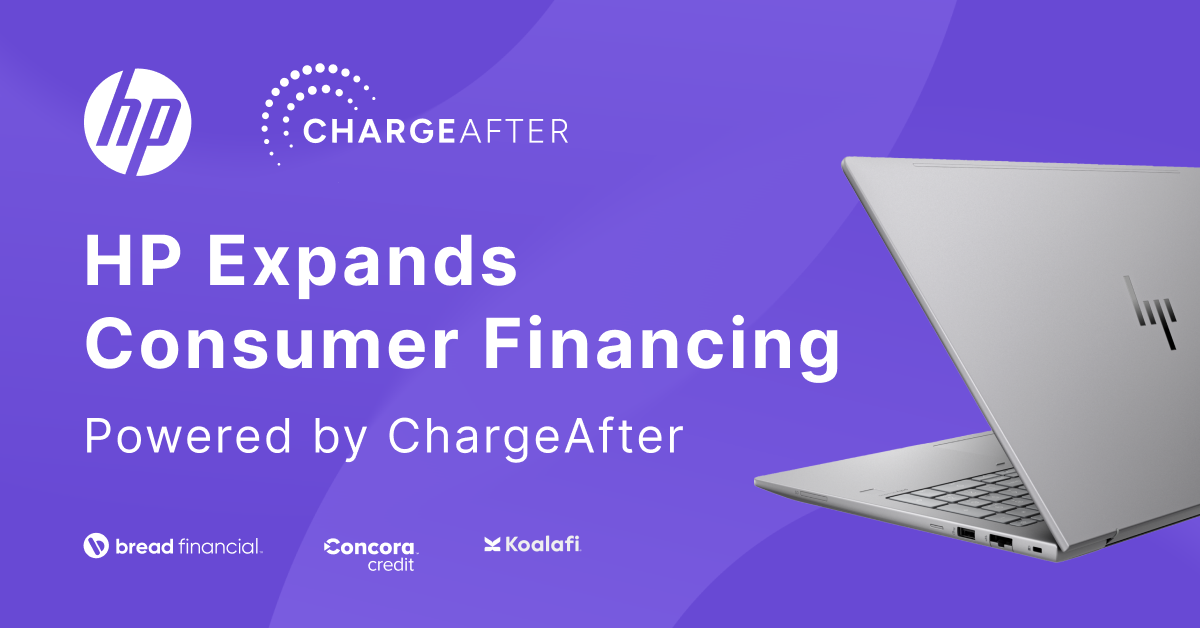

We are thrilled to share that ChargeAfter is the technology provider behind HP’s newly expanded consumer financing offering This exciting collaboration empowers nearly every U.S. consumer with the purchasing power to acquire their favorite HP products through flexible financing options available on HP.com.

HP’s new consumer financing program leverages ChargeAfter’s cutting-edge technology and network of lenders, with Bread Financial, Concora, and Koalafi providing financing options for consumers across all credit tiers. In a single online application, consumers are instantly matched with the most suitable lender for their specific needs, thanks to our sophisticated waterfall technology.

Additionally, ChargeAfter’s platform simplifies the management of post-sale transactions and communications with lenders, providing the HP team with comprehensive visibility, control, and access to detailed analytics and insights.

The collaboration with HP showcases ChargeAfter’s pivotal role as a partner in revolutionizing point-of-sale financing for major retailers.

Consumer finance is not set to grow. It’s growing! As consumer behavior shifts towards online shopping, the benefits of eCommerce financing are becoming increasingly evident. By offering flexible payment options, ecommerce financing empowers customers to make purchases they might otherwise defer, significantly boosting conversion rates and reducing cart abandonment. For retailers, this means increased sales and the ability to reach a wider audience, including those needing access to traditional credit. Additionally, ecommerce financing can foster greater customer loyalty, encouraging repeat purchases through convenient and accessible payment plans. This trend aligns with the broader growth of POS financing, illustrating the critical role of flexible payment solutions in modern retail strategies.

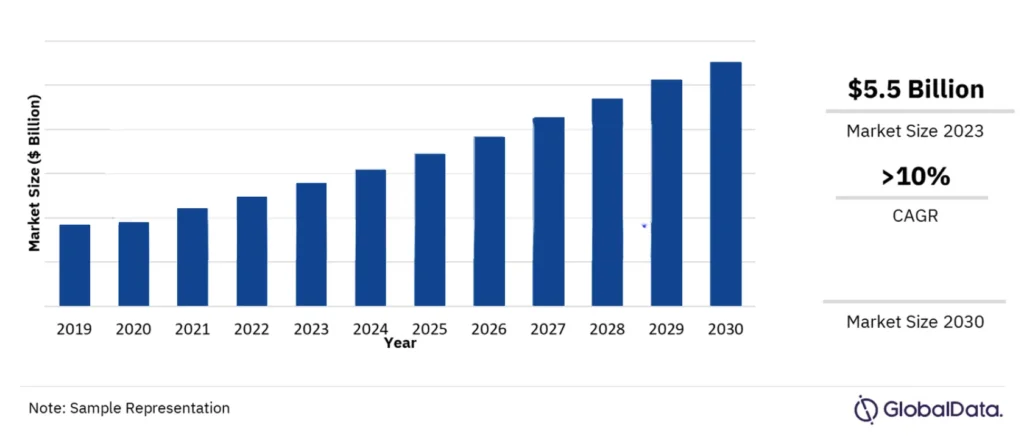

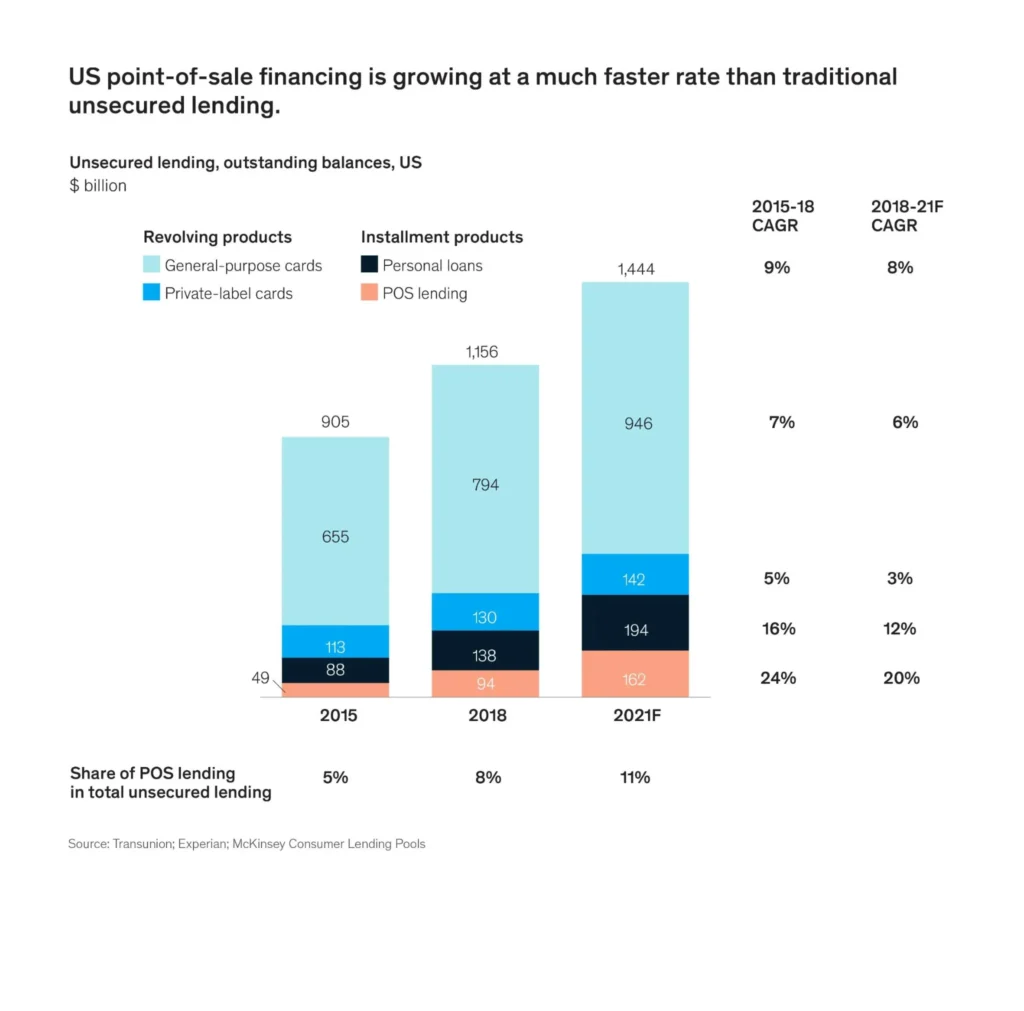

According to recent data from Globaldata, (POS) point-of-sale financing continues to grow significantly within the total unsecured lending balances in the United States. As of 2023, credit card balances amounted to around $1.08 trillion, reflecting a substantial increase from previous years. The POS software market was valued at approximately $5.5 billion in 2023 and is projected to grow at a compound annual growth rate (CAGR) of over 10% through 2030. This growth is primarily driven by the rising adoption of contactless payment methods, which are favored for convenience, speed, and safety. The retail sector remains the leading end-user segment within this market, highlighting the expanding influence of POS financing.

POS software market outlook 2019-2030 ($ Billion)

Market size ($ Billion)

Similarly, according to McKinsey Consumer Lending Pools, the same trend is can be seen internationally with POS financing making up 11%

Prudence Research has also shown, how BNPL, a financial instrument for short term installment loans, falling within the POS Finance umbrella, has grown and how it is forecasted to grow dramatically in the coming years.For instance, the Buy Now Pay Later market size is forecasted to grow to a staggering 3.2 Trillion dollars by 2030.

Financing can expand the customer base for various purchases, including appliances, electronics, furniture, home improvement projects, and services like elective medical procedures and dental equipment and procedures. Offering financing options can boost sales for any seller, whether in a brick-and-mortar store, online, or through a call center, and cater to all consumer types.

Buying a product or service that costs between $1,000 and $10,000 is more complex than making a $50 purchase by swiping your credit card. Businesses need to make an effort to attract a broader range of consumers.Through embedded finance, consumer financing has expanded beyond buy now, pay later and adopted long-term installment payment, 0% APR, revolving lines of credit, and more, to offer consumers flexible payment options.

Industry analysis found how consumer financing increases merchant sales. For instance:

According to The Inaugural Citizens Point of Sale Survey by Citizens Financial Group, the most notable finding is that 76% of consumers are more likely to make big-ticket sales when given the option of consumer financing, such as BNPL or other payment plan options. Of those surveyed, 66% want consumer finance alternatives to credit cards.The survey revealed that consumers would prefer non-credit-card consumer financing with fixed monthly plans, clear payment terms, and a clear understanding of how the amount will be paid off as the most important factors when considering a large purchase.

Comparably, a study by Futurepay.com reports that 56% of shoppers are more inclined to purchase a high-priced item online if financing options are available. This percentage increases to 73% for frequent online shoppers. These statistics are very close to findings by the Citizens Financial Group.

A recent FREE retailer insights survey by ChargeAfter indicates that from a retailer’s perspective, 85% of retailers expect year-on-year growth in consumer financing.

Higher value, more sales with ecommerce financing options

Merchants selling higher ticket items who offer consumer finance options achieve more sales than merchants without consumer financing options.

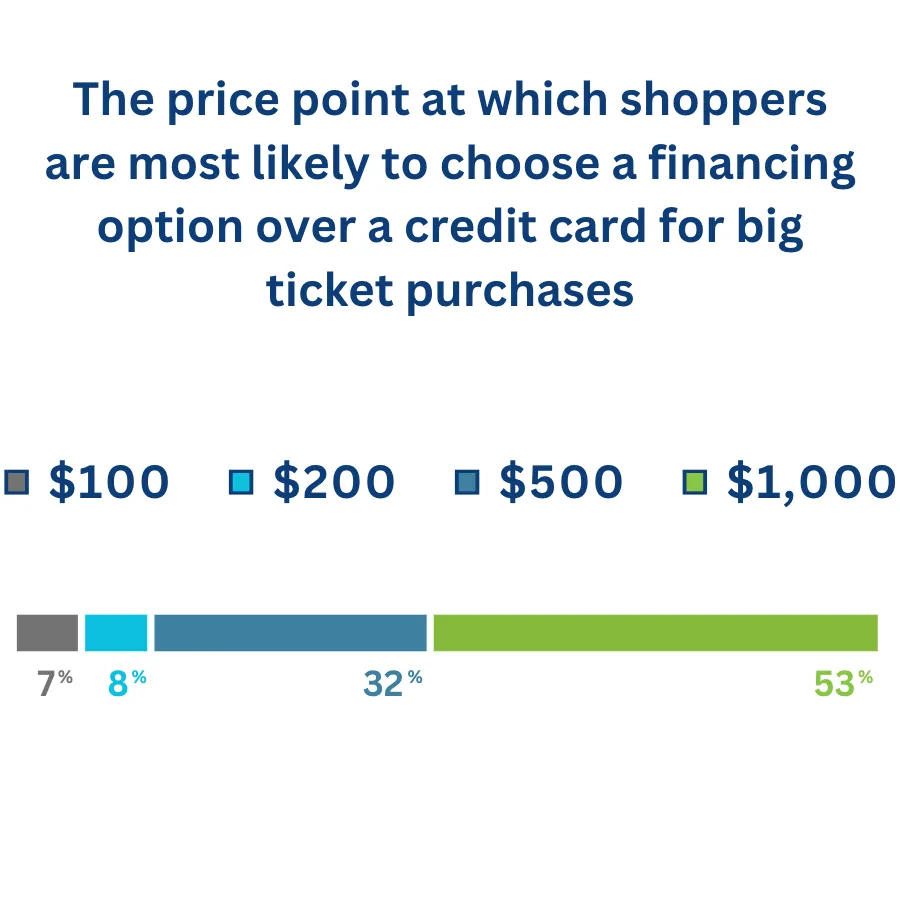

‘The Big Ticket: What’s stopping Shoppers’ (big-ticket survey) published its findings and according to them, financing alternatives stimulate high-value purchases. Over two-thirds of shoppers (68%) and 79% of daily shoppers would be more inclined to purchase a high-priced item if they could divide the cost into smaller payments. For high-priced items under $1,000, almost half of all shoppers (47%) prefer alternative financing over a credit card to complete the transaction. Even at a price as low as $200, 15% of shoppers were willing to switch away from a credit card.

Similarly, ChargeAfters’ Retailer survey released in 2023, from a retailers’ perspective, states that merchants recognize that financing options drive big-ticket purchases.

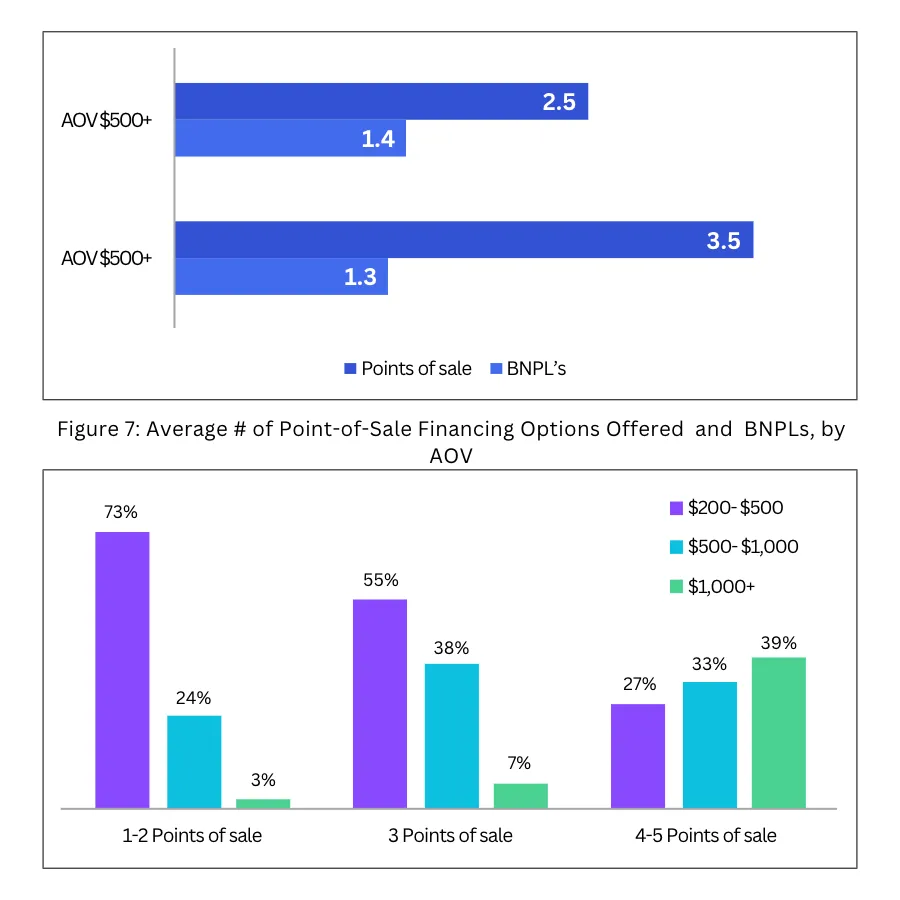

The number of BNPLs merchants offered to customers is not affected by the retailers Average Order Value (AOV). However, other POS financing options vary significantly depending on the AOV of the business. When the AOV is less than $500, companies typically offer 2.5 different POS financing options. However, when the retailer AOV exceeds $500, this number increases to 3.5 different POS financing options. As their AOV increases, merchants seek to diversify their payment options to meet customer demands. There is no one-size-fits-all solution regarding financing options, particularly with a substantial AOV. Offering a limited BNPL of pay in four or six installments is insufficient as customers require more flexibility and choice.

Financing options by average order value (AOV)

Fintech companies at the forefront of consumer finance innovation offer embedded financing & lending technologies making it easier for merchants to integrate omnichannel consumer financing solutions. Embedded finance solutions that integrate easily, such as ChargeAfters’ multi-lender platform, allows merchants to offer their customers quick, convenient, and personalized financing options.Customers connect to a wide choice of financial products and lenders in a single application, resulting in an 85% approval rate. Merchants increase sales by offering consumer financing and installment payments on sales where the same customers would typically walk away from the sale.

Reduce cart abandonment with consumer finance

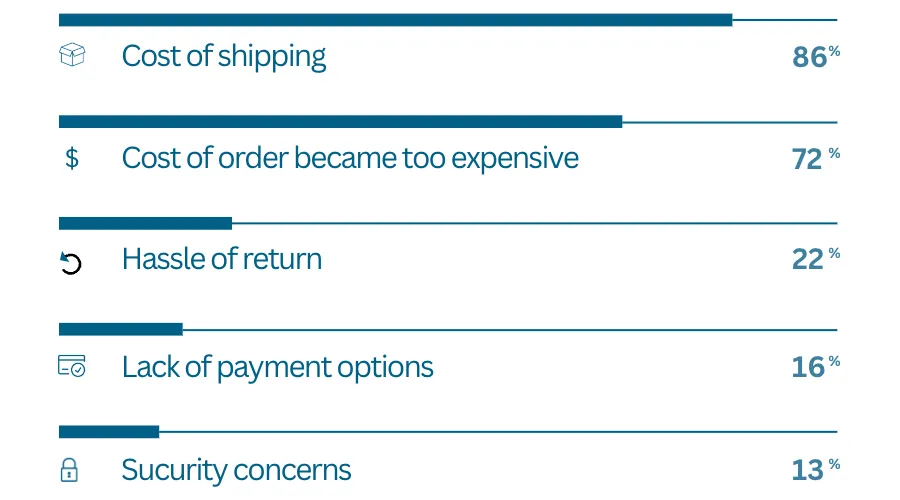

The Big Ticket: What’s stopping Shoppers survey found that 66% of shoppers abandon their carts after adding an item to their shopping cart. 72% of this abandonment was due to the items being too expensive, and 16% because there were no payment options.

Another Research conducted by beymard.com in 2022 shows that site trust (18%), complicated checkout process (17%), inability to calculate total order cost upfront (16%), not enough payment options (9%) and. Credit card declines (4%) are the main reasons for abandonment. These statistics can be significantly improved with the correct embedded finance technology.

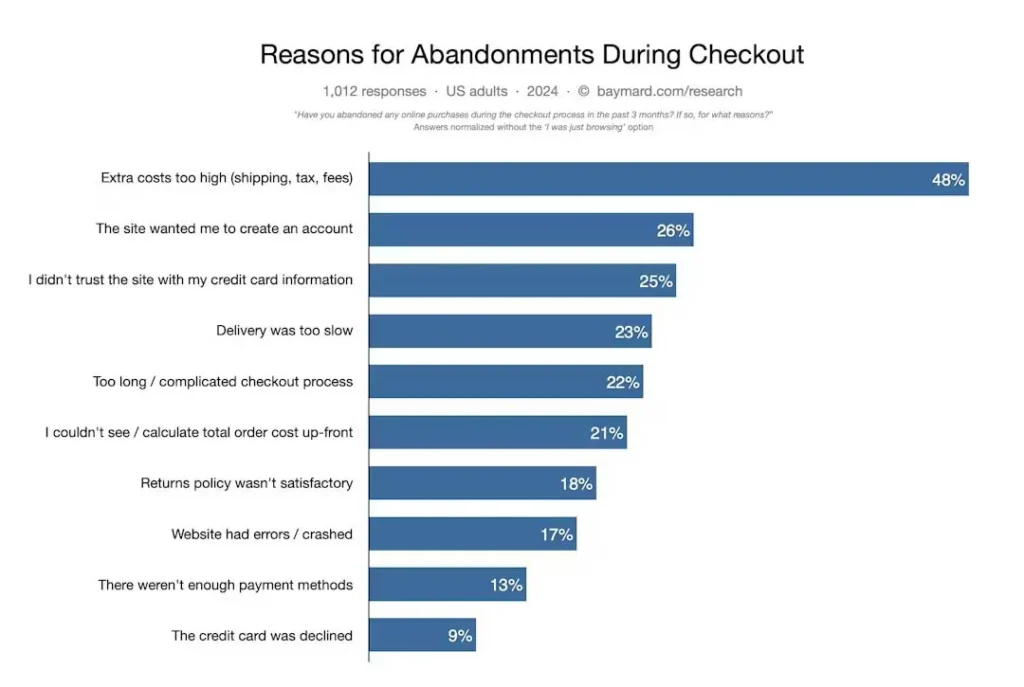

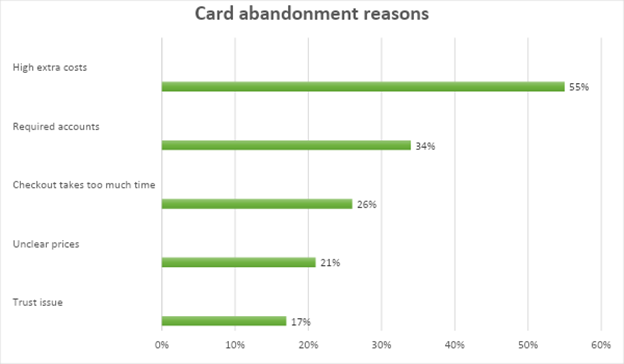

According to recent research conducted by Baymard Institute in 2024, the main reasons for cart abandonment include high extra costs (48%), the site requiring account creation (24%), slow delivery (22%), lack of trust in the site’s security (18%), complicated checkout processes (17%), inability to see total order costs upfront (16%), and insufficient payment options (9%). Credit card declines account for 4% of abandonments. These issues can be significantly reduced with the correct embedded finance technology.

With an embedded lending platform like that of ChargeAfter, merchants can increase sales by decreasing cart abandonment.

Conclusion: Boost sales with ecommerce financing

Reducing cart abandonment is one of the most significant benefits of offering consumer financing and installment payments in e-commerce stores. Many customers abandon their carts because they need help to afford the full price of an item at the time of purchase. However, by offering financing options, merchants can make sales more affordable and accessible, reducing the likelihood of cart abandonment and increasing the chances of a sale.

In addition to reducing cart abandonment, offering financing options can increase customer loyalty and repeat business. Customers who take advantage of financing options are more likely to return to the same merchant for future purchases, as they have established a relationship and trust with the merchant through the financing process.

Offering ecommerce financing options can help merchants reach a wider audience of potential customers. Many consumers who may not have been able to afford high-ticket items in the past may now be able to do so with financing options, opening up a whole new market for the merchant.

Finally, offering financing options can help merchants stand out from the competition and differentiate themselves in the crowded e-commerce marketplace. By providing financing options, merchants can provide a more comprehensive and customer-centric shopping experience that distinguishes them from other retailers.

Digital technology has disrupted the way retailers construct their marketing strategies and how customers shop, which is why the world of retail is very different today than it was just five years ago. Consumers now use their smartphones to see product reviews and compare prices. In other words, making informed decisions is much simpler for consumers. The same is true for the financial component. The form of retail financing the buyer chooses has changed due to advances in consumer financing over the past few years.

For example, the usage of point-of-sale (POS) financing increased drastically after the pandemic hit, and the trend is still going strong as BNPL and other POS financing options have become a habit for consumers. Recent data shows that BNPL is evolving beyond a mere payment option, According to McKinsey & Company, about 17% of Afterpay users initiated one or more transactions directly through the app in February 2021. This shift illustrates the evolving role of retail financing in the consumer shopping experience. As shopping patterns change, brands can develop and apply next-generation tactics to enhance the customer experience with different consumer financing options in the upcoming years.

Why is consumer financing necessary?

Retailers need help selecting the best retail financing options due to the wide range of choices available.

So why is retail financing so necessary?

To increase sales – you can offer customers lower interest rates, promotions, or discounts on your products. However, it’s becoming more attractive to consumers to pay full price if they have the option to finance their purchase and split the payment. Using lending services has become a part of our merchant offering and consumers’ lives.

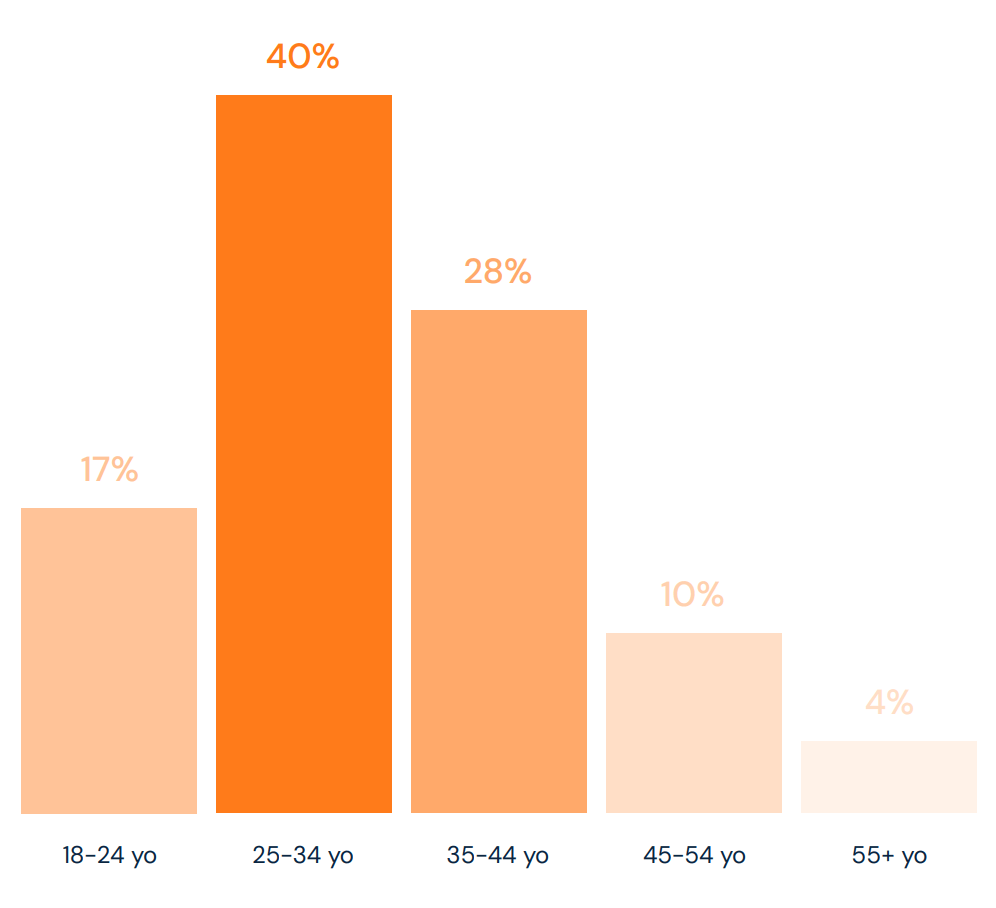

In addition, customers can split payments over time without incurring any costs, thanks to current financing solutions. Because of this, BNPL lending and POS financing are among the most popular types of retail financing available today. According to data from Fit Small Business, 56% of millennials and 40% of consumers aged 25-34 have used BNPL services, making them the most significant demographic for BNPL. This trend is particularly pronounced among consumers earning between $20,000 and $50,000 annually, with 21% of this income bracket using BNPL last year.

Because of this, retail financing options are now available as an integral part of the shopping experience for products and services like furniture, home improvement, vacation, auto parts, education, and many more.

Rising popularity of omnichannel consumer lending

Consumer financing has become more popular overall during the past ten years. More consumers frequently use retail financing services to obtain the funds required for shopping or unexpected expenses. According to the statistics, consumers favor point-of-sale financing solutions. Retail financing choices give consumers freedom, making it much easier for them to manage their finances if used appropriately. Recent insights from McKinsey & Company highlight that POS financing providers are now not just payment partners but also integral to commerce enablement and co-marketing, particularly in omnichannel strategies.

Retailers today must ensure that their financing options are seamlessly integrated across both online and offline channels. Consumers expect a smooth transition between their digital shopping experiences and in-store visits, making it essential to provide a consistent financing experience. However, many retailers need help achieving this uniformity, which can lead to customer dissatisfaction or even lost sales. Retailers can effectively bridge this gap by adopting strategies such as integrated POS systems and maintaining consistent credit terms. Leading retailers who have embraced these strategies deliver the same convenience and flexibility, regardless of whether customers shop online or in-store. This approach enhances customer satisfaction, strengthens loyalty, and encourages repeat business. However, online retail financing is one of many instruments that can help buyers have a positive purchasing experience. Customers who prefer local shopping or need a nearly complex product to select or purchase online require retailers to adjust to their needs.

For instance, if a customer wants to purchase a new mattress or any other type of furniture, they may want to physically inspect it to ensure they are making the appropriate decision. Therefore, when a customer went to a store after seeing the retailers’ online pleasant retail financing options, they had to have the same financing experience. For situations like that, retailers offer in-store retail financing. To provide the buyer with the same comfortable shopping experience, several furniture stores, including Raymour & Flanigan, are now leveraging POS financing and BNPL lending features via an omnichannel multi-lender platform.

Point-of-Sale financing

POS financing has evolved into one of the critical tools for consumers, making it seamless to access flexible lending options. Younger generations are particularly inclined towards these methods, with BNPL being a significant driver. Technological advancements and deeper integration into the shopping experience have marked the rise of POS financing services. According to McKinsey & Company, POS financing providers now leverage advanced technological capabilities, such as sophisticated fraud detection models and deep integrations into shopping carts, to enhance consumer service and mitigate risks. These advancements are crucial for maintaining the effectiveness of retail financing solutions in a competitive market.

The fact that customers receive the quickest and coziest method of financing is one of the reasons the service has become so well-liked. It usually only takes a few seconds to apply and receive the funds you require when reputable third parties are involved. It also allows customers to receive the best financing options: Installments, Revolving loans, BNPL, or LTO (lease-to-own), among the most popular examples of financing.

Potential problems for retailers

Retailers will probably have to contend with a continued challenging growth environment and higher expenses while offering solutions for their customers who are operating with cash constraints.

3 Strategies for retailers to tackle consumer financing demand

1. Be on every channel

According to TIDIO statistics, customers utilize POS financing and BNPL differently in-store and online. All customers do not prefer online services. Some customers prefer to purchase goods and services from brick-and-mortar establishments.

This demonstrates the need for consumer financing solutions like POS financing or BNPL lending across all channels. Whether it will be for customers who choose to shop in person at the neighborhood store or for online users on websites or mobile applications, retailers need to ensure they are present on every channel to meet the diverse needs of their customers. Retail financing must be integrated into digital and physical platforms to provide a seamless experience that meets consumers wherever they shop.

2. Offer simple and clear financing

According to the findings of Citizens Point of Sale Survey, 76% of American consumers are more inclined to make a retail sale if a payment plan is supported by an easy and smooth point of sale experience. The survey found that 62% of respondents would like fixed monthly contracts with unambiguous payment terms, and a good understanding of how the sum will be paid off as the most crucial elements. Additionally, 66% of customers believe they already have sufficient credit cards and would rather avoid adding an additional credit card merely to make a large purchase. This suggests that customers seek a different option than applying for a new credit card to make a sizable purchase at a store. Retail brands can modernize their payment solutions by moving away from the store credit approach and adding simple financing options to their customers.

3. Offer white-labeled consumer financing

Consumers are flocking to private-brand products in the current market to combat inflation. Retailers should periodically reevaluate their category strategies to take advantage of this. Successful stores will strike a balance between fast-changing consumer tastes and pressures from individual inflation rates. This would require reconsidering their balance of national and private brands.

Consumers planning a significant purchase view trust in the organization providing the financing as one of the main reasons they prefer branded lending platforms over independent FinTech firms. This demonstrates how retailer brands can profit from branded white-label financing solutions to attract more customers.

Additionally, financing platforms like ChargeAfter provide customizable white-label financing options. This allows the merchant to change the financing software however they see fit while giving customers the financing options they need and demand. By offering white-labeled retail financing, retailers can build stronger brand loyalty while providing trusted and customized financial solutions to their customers.

How to choose the best consumer financing company for your store

Ready to provide your clients with immediate financing? Great! But which should you pick? It’s difficult to single out the top consumer financing providers because so many fintech firms provide BNPL products. Having said that, there are some qualities to consider while selecting a BNPL and consumer financing providers:

Positive customer experience: Businesses need to deliver satisfying user experiences. For instance, ensuring a smooth checkout experience would help prevent cart abandonment. Since over 80% of shoppers leave their carts empty before making a purchase, financing and BNPL ought to have superb integration into your customer journey. User-friendly features, and no interruptions during checkout help decrease cart abandonment.

Perfect payment plans: By offering various payment options, retailers open up their products to more people, which can increase sales and brand loyalty. Customers and business owners alike can benefit from high flexibility. Thanks to financing platforms, any retailer can act as a lender. A financing platform gives shoppers the freedom to choose their financing conditions based on sophisticated risk assessment models. Customers will be able to select from a variety of payment plans without having to worry about not being approved.

Reduced risks: Flexibility and scalability are features reputable consumer finance businesses can provide. You may increase sales, draw in new clients, and maintain existing ones by making it simple for people to finance the goods and services, but risk management should always be considered. Make sure to work with providers with low MDR (Merchant Discount Rate) and can provide the best interest rate for your customers. In addition, make sure the PoS financing solution of your choice has cutting-edge management including managing reconciliation, chargebacks and dispute resolution. Working with multiple lender increases redundancy as well as enabling personalization and choice.

Helps you control Data: Lastly, reputable BNPL and POS financing solutions should assist retailers in regaining control over consumer data and streamlining payments. This would enable retailers to understand better what customers want, need, and like. Advanced financing solutions permit retailers to give clients financing options, safeguard user information, and build long-lasting relationships with customers.

Summary

Retail financing is evolving and brands must stay on top of emerging trends to ensure they offer the services that customers want. The best way to do this is through a platform-first approach. As highlighted by recent data from McKinsey & Company, POS financing providers are integrating more profoundly into the shopping experience and expanding their service offerings to include traditional banking products. Retailers and retail financing platforms must work closely together to ensure they provide seamless, flexible, and secure financing options that meet the needs of today’s consumers.

Retail financing solutions have become critical to modern retail strategies. Retailers who successfully implement these advanced financing strategies— through an omnichannel approach, white-labeled, and improved risk management—will likely find themselves better positioned to capture consumer loyalty and drive long-term growth, even in a competitive market. Therefore, it is not just about offering financing options but about integrating retail financing into the broader retail strategy to enhance the overall customer experience and meet evolving consumer expectations.

About ChargeAfter

ChargeAfter is a leading multi-lender platform for Consumer Financing. It connects businesses with the most reliable lenders, enabling them to offer customers the greatest financing solutions. With the best system of Waterfall Financing, ChargeAfter guarantees lending to every shopper, by matching the most relevant lender to every client. Using the unique consumer financing technology, ChargeAfter provides consumers with the best shopping experience. MUFG, VISA, Bradesco, BBVA, Synchrony, CITI Banks are among the investors of ChargeAfter.

E-commerce financing has transformed how customers approach high-end purchases, particularly in fashion. While some companies thrived during the pandemic, many luxury fashion and skincare brands saw declining sales. One major factor is the gap between price and flexible payment options, which remains challenging for these brands.

Fashion is a fast-paced industry that continually evolves to meet consumer demands. Younger generations, the most eager to stay on trend, often find luxury fashion unattainable due to the high prices. Additionally, they refrain from accumulating debt through traditional credit and in-store cards.

How price flexibility helps customer acquisition

Offering financial flexibility through buy now, pay later (BNPL) solutions bridges the gap between price and accessibility. With rising job losses and student debt, younger consumers—who frequently update their wardrobes—seek flexible solutions to manage their spending. Brands like Nike and Urban Outfitters have embraced BNPL white-label solutions, allowing customers to purchase without upfront costs.

This shift helps fashion retailers expand their customer base, increasing brand loyalty without lowering prices. Instead, brands can provide payment flexibility through POS financing platforms to attract more customers.

How price impacts cart abandonment in fashion

Cart abandonment is a significant issue in online fashion, and price is often why customers abandon their carts. Introducing embedded lending networks and in-store financing options has provided an effective solution. By spreading the cost over several months through POS lending, customers are more likely to follow through with purchases.

The global online fashion industry is expected to generate $7 billion in online sales by 2022. To stay competitive, fashion retailers must reduce cart abandonment rates, which can be achieved by incorporating embedded finance platforms that offer flexible payment solutions.

Increasing sales without lowering price through BNPL

Luxury fashion brands can grow sales without lowering prices by offering BNPL and white-label POS systems. By integrating embedded lending platforms into their e-commerce stores, brands allow customers to finance their purchases over time. This helps customers manage large purchases and ensures that brands maintain their product value.

Statistics have shown that introducing BNPL white-label solutions has led to a significant reduction in cart abandonment and an increase in average order value (AOV). Fashion brands that have adopted these omnichannel financing solutions see lower customer acquisition costs and higher customer retention.