How Lender Orchestration Is Reshaping Consumer Credit

| Lender orchestration is transforming point-of-sale financing. Rather than depend on a collection of individual financing programs, orchestration enables merchants to implement intelligent, real-time multi-lender financing flows designed to maximize approvals, improve customer experience, and create greater checkout resiliency. |

What you’ll learn

- Why relying on a single lending partner exposes merchants to hidden risks

- How lender orchestration helps maintain financing continuity as credit markets shift

- How different lending programs are matched to different consumer profiles and transaction types

- Why network-based financing is becoming a strategic advantage for enterprise commerce

What is lender orchestration and why does it matter?

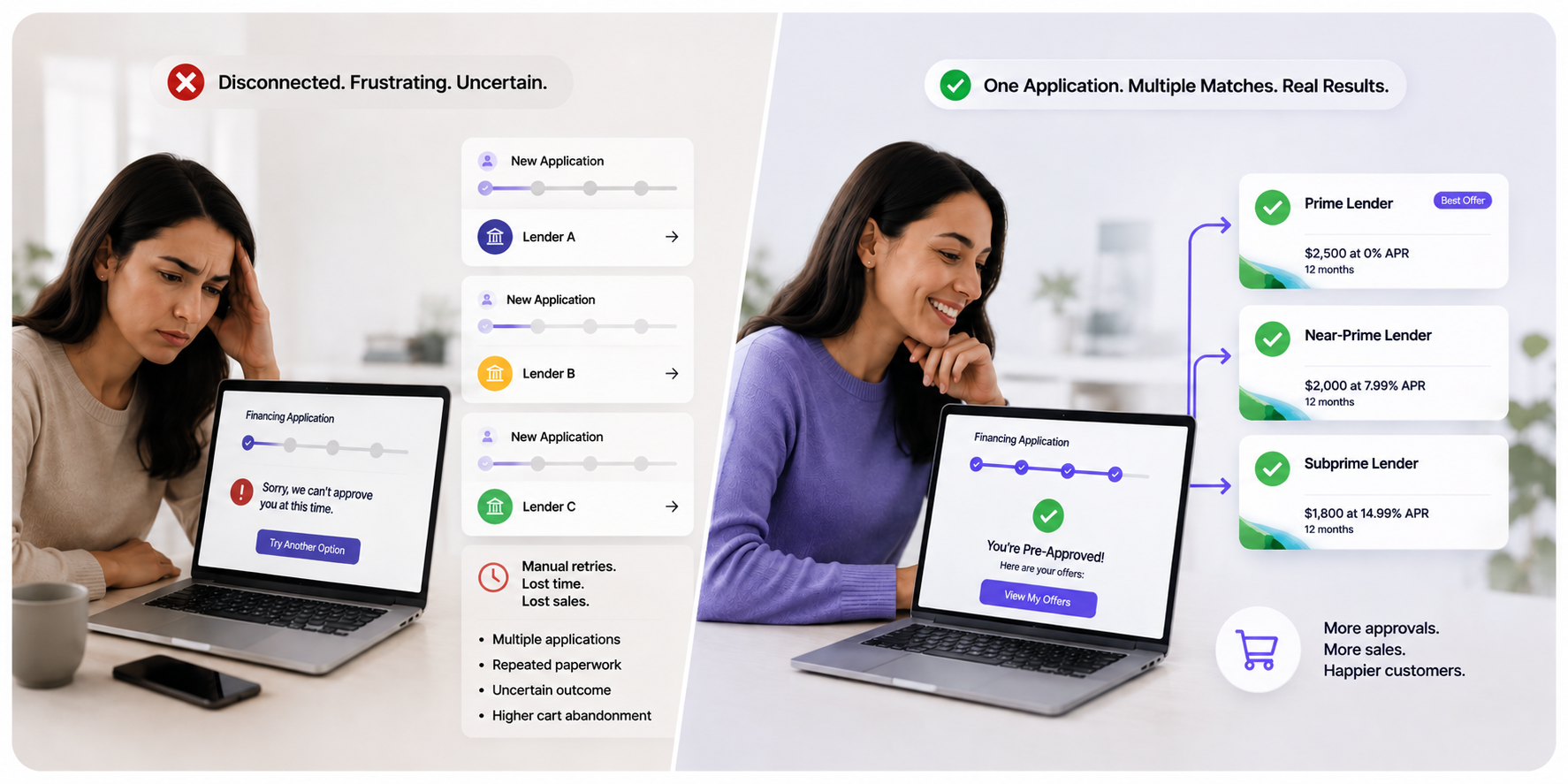

Lender orchestration involves a technology infrastructure that dynamically routes financing applications to multiple lenders, matching customers with suitable financing options in real time. It matters because no single lender can effectively serve every customer across credit tiers, transaction sizes, or in all market conditions.

By leveraging a network of financing providers, lender orchestration expands financing access while giving customers personalized financing options at their moment of need.

| Lender orchestration | A technology layer that connects merchants to a network of financing providers, automatically matching consumers to the most suitable lender based on credit profile, transaction size, and real-time lender availability. |

| Point-of-sale (POS) financing | Credit or payment options offered directly at the point of purchase, allowing shoppers to spread payments over time rather than paying in full upfront. |

| Multi-lender network | A financing ecosystem that includes multiple lending partners, each with different credit appetites, products, vertical specialization, and customer segments, working together through a single integration. |

Point-of-sale (POS) financing is undergoing a structural shift. What began with traditional in-house retail credit cards expanded into a fragmented ecosystem of standalone lenders. Think about: Buy Now, Pay Later (BNPL) leaders such as Klarna, Affirm, and Afterpay, alongside established financial institutions like Citi and Wells Fargo, and hybrid providers like Bread Financial.

While that expansion increased consumer choice and financing access, it also created new challenges for merchants. Shoppers expect experiences that are personalised, frictionless, and delivered in real time. Yet delivering that experience requires multiple lender relationships, each with its own technology, underwriting criteria, and operational requirements. The result is a fragmented financing ecosystem that consumes resources, complicates optimization efforts, and leaves merchants exposed when individual lenders tighten credit standards or change strategic priorities.

Lender orchestration is the structural response to those competing demands.

Do consumers still choose financing based on the lender’s brand?

| Brand trust still matters, but there are other considerations. Merchants are increasingly evaluating financing partners based on factors beyond consumer recognition, including credit reach, flexibility, and checkout resilience. Today, lenders operate within broader commerce ecosystems where both the financing provider and the overall customer experience contribute to success. |

Historically, merchants selected financing providers partly based on brand recognition. The assumption was that customers would feel more comfortable with lenders they already knew and trusted, particularly for high-ticket and long-term financing.

That dynamic is shifting. Consumers do care about who provides financing, but they also expect instant approvals, transparent payment terms, and no-friction checkout experiences. As embedded finance matures, the lender is increasingly one component of a larger merchant-controlled experience.

This is changing how merchants structure financing programs. Rather than choosing lenders to serve every customer and every transaction type, brands are adopting a network-based approach that connects customers to the financing solutions best matched to their needs. In this model, lenders continue to play a critical trust and underwriting role while contributing specialised capital within a broader network.

Why is credit appetite more volatile than consumer demand?

| Lender willingness to extend credit does not move in parallel with consumer demand. When economic conditions change, funding costs rise, or investor sentiment shifts, lenders tighten underwriting standards, reduce exposure to certain risk segments, or narrow promotional programs, often with little or no visibility to merchants. |

One of the most overlooked risks in consumer financing is the assumption that lender appetite remains constant over time. Merchants can interpret declining approval rates as weakening demand. In reality, the two forces operate independently.

Many non-bank lenders depend on external capital sources to fund originations. When economic conditions change, those funding costs fluctuate, and lenders respond by adjusting their underwriting criteria. A customer who qualified for financing several months ago may receive a decline from the same lender today, not because their circumstances changed, but because the lender’s risk tolerance did.

As financing becomes a larger driver of conversion and revenue, reducing dependence on any single lender’s underwriting strategy is becoming a baseline requirement rather than a competitive advantage.

What factors cause lender credit appetite to shift?

- Rising interest rates increasing the cost of funds for non-bank lenders

- Tightening capital markets reducing the availability of lending capital

- Regulatory changes affecting underwriting requirements or permissible products

- Portfolio performance deterioration prompting lenders to tighten risk thresholds

- Investor sentiment shifts reducing lender appetite for certain consumer risk segments

How does orchestration create resilience in an unpredictable market?

Orchestration transforms financing from single-provider relationships into a diversified network model. When one lender becomes more conservative, another may continue serving that customer segment. When market conditions affect one product, alternatives remain available. The result is a financing program that adapts without requiring merchants to reconfigure their checkout strategy.

| Financing resilience | The ability of a merchant’s financing program to maintain consistent financing access and approval rates across changing lender strategies, credit market conditions, and economic environments. |

Conversations about multi-lender financing often focus on approval rate optimization. While that is a tangible benefit, another strategic case for orchestration is resilience.

Historically, merchants treated financing as a vendor relationship. A lender was selected, integrated, and expected to support its customer base over time. That model assumes lender appetite is relatively stable. Increasingly, that assumption does not hold.

The challenge for merchants is not predicting when lender appetite will change. It is maintaining financing availability when it does. A financing program built around a single lender remains exposed to that lender’s underwriting decisions, even when consumer demand remains strong.

Lender orchestration addresses this by building redundancy into the financing infrastructure. Rather than relying on one source of financing merchants access multiple providers with different credit appetites, risk models, and products. The checkout experience remains consistent for consumers even as the underlying lender network adapts to market conditions.

In that sense, orchestration is not simply a conversion tool. It is infrastructure designed to create stability in an inherently dynamic credit environment.

How does orchestration match lending to consumer profiles?

Effective orchestration routes consumers to the financing solution best aligned with their credit profile and transaction type. Not every financing product is optimized for every borrower. Orchestration automates matching in real time, across the full credit spectrum, without requiring merchants to determine which lender should serve which customer.

Resilience comes not only from having multiple lenders, but from having access to different forms of financing designed for different customer segments.

Rather than requiring merchants to manually determine which lender should serve which customer, orchestration automates these decisions in real time, drawing on each provider’s specific strengths across the credit spectrum.

Key takeaways

- Credit appetite can change faster than consumer demand, creating hidden merchant exposure

- Reliance on a single lender creates vulnerability to underwriting and funding shifts

- Multi-lender networks help merchants maintain financing continuity across changing market conditions

- Orchestration enables access to specialised forms of capital across the full credit spectrum

- Financing resilience is becoming as strategically important as financing availability

- The checkout experience remains consistent for consumers even as the lender network adapts behind the scenes

- The future of consumer financing will not be defined by any single lender, financing product, or underwriting model. It will be shaped by networks that intelligently connect consumers, merchants, and capital providers in real time.

What does this mean for enterprise merchants?

| For enterprise merchants, lender orchestration represents more than increased approval rates. It is a strategy for building resilience into the financing experience, reducing dependence on individual lenders, and ensuring consumers always have access to relevant financing options regardless of how credit market conditions change. |

As financing options proliferate and lender appetites continue to shift, merchants that adopt network-based financing models will be better positioned to deliver consistent customer experiences and sustainable long-term growth.

Merchants that continue to rely on single-lender relationships are, in effect, taking a structural risk: not on consumer demand, but on one organisation’s willingness to extend credit. Orchestration eliminates that single point of failure.

Frequently asked questions

Buy Now, Pay Later (BNPL) is a specific financing product, typically a short-term, interest-free installment plan for smaller purchases. Lender orchestration is an infrastructure layer that can include BNPL as one of multiple available financing options, routing consumers to the most appropriate product based on their profile and transaction size.

From the consumer’s perspective, lender orchestration is largely invisible. They see a financing offer suited to their profile and transaction. Orchestration operates behind the scenes, routing the application to the most appropriate lender in real time, which typically results in higher approval rates and more relevant financing terms.

Yes. Orchestration platforms can integrate existing lenders, as long as both parties agree. This lets merchants retain their current lender/s while gaining access to additional providers, which reduces single-lender dependency without requiring a full infrastructure rebuild.

Enterprise merchants with high transaction volumes, diverse customer credit profiles, and big-ticket average order values see the most immediate benefit. Early adoption of financing orchestration was driven by furniture, mattress, electronics, and other retail sectors. Today, home improvement is leading the next wave of adoption.