What to Do When Your POS Financing Provider Exits the Market – ChargeAfter

Even the most trusted financing providers can change direction. The key for merchants is preparedness, with a built-in strategy for lender redundancy, control, and long-term stability.

Lenders can change direction for various reasons, from shifting business priorities to changing market conditions, or strategic exits from specific products or industries. Losing a lender provides an opportunity for merchants to rethink their financing model and adopt a more stable, scalable, and resilient approach. With the right technology, what starts as disruption can become a turning point toward a smarter financing strategy built for stability, control, and growth.

1. Why Replacing one POS Lender with another isn’t a Long-Term Solution

When you rely on individual lenders, any shift in strategy, whether a tightening of terms or a full market exit can leave your business exposed. It’s not just about losing a financing option, it’s the operational headache of finding a suitable replacement, negotiating new terms, managing compliance and integrations, and getting internal teams aligned fast enough to avoid gaps in service.

Swapping one provider for another might seem like a quick fix, but it repeats the same pattern of dependency and doesn’t solve the underlying problem: lack of control. Merchants need more than a replacement—they need a better solution. One that offers continuity, flexibility, and the ability to adapt as lender dynamics change.

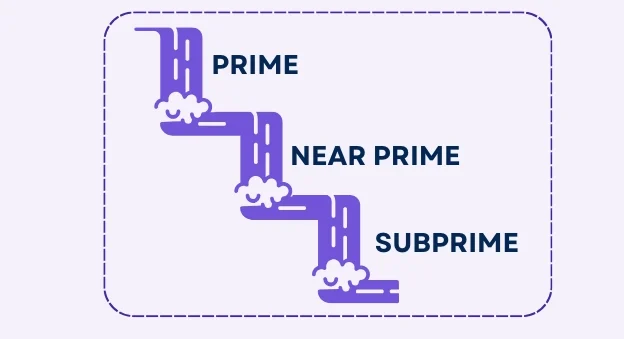

2. How Waterfall Financing Transforms POS Lending

While many merchants already work with two or three lenders, these relationships are often siloed, requiring multiple applications and inconsistent customer experiences. This fragmented approach leads to operational inefficiencies, a fractured customer experience, and missed sales opportunities.

Waterfall financing solves this by using technology to unify the process. With a single application, customers are automatically routed through a sequence of lenders based on their credit profile. The result is a smoother experience, higher approval rates, and broader financing coverage.

3. How to expand your lender network without adding complexity

Traditionally, adding lenders to your POS financing program has meant more complexity: more integrations, more coordination, and more pressure on already stretched teams. That’s why many merchants have stayed limited to one or two providers, even when they know their customers could benefit from a broader range of options.

Waterfall financing not only improves the customer experience—the technology that enables it creates the foundation for easier, smarter lender management. With the right infrastructure, merchants can route applications intelligently across multiple lenders without building or maintaining separate integrations. The result: broader credit coverage and product choices with less operational strain.

4. How a Platform Approach Puts Merchants in Control of POS Financing

Beyond improving lender redundancy and the checkout experience, a platform-based model delivers additional powerful advantages for merchants before, during, and after the sale. With all lenders operating through a single interface, you gain real-time visibility into performance metrics, approval rates, and customer behavior across channels.

Managing post-sale activities such as disputes, reconciliation, and communication with lenders becomes significantly easier when everything flows through a single interface. No more jumping between portals, coordinating with multiple lender reps, or manually pulling reports.

More importantly, a platform gives you control. You can configure lending rules, manage promotions, add new products, or make changes in response to business needs, without depending on IT to rebuild workflows from scratch. It’s the kind of flexibility and stability that’s simply not possible when working with disconnected lenders in siloed systems.

5. The Business Impact of Smarter POS Financing Across the Board

Shifting to a platform-powered, waterfall-based financing model isn’t just about reducing risk—it’s about unlocking real business value. Merchants who adopt this approach consistently see higher approval rates and a smoother path to purchase for customers across the credit spectrum.

Internally, teams benefit from simplified operations, faster onboarding of lenders, and greater visibility across their entire financing program—from performance metrics to post-sale servicing. When financing works seamlessly, it stops being a source of stress and becomes a true driver of growth.

In moments of change, this model offers what single-lender setups can’t: stability, flexibility, and the confidence to move forward without disruption.

Building a smarter financing strategy starts with ChargeAfter

In my work with merchants and lenders every day, I see the difference that ChargeAfter’s platform can make, especially when a lender exits or tightens its terms. It’s not just about finding a replacement: it’s about building a financing program that’s resilient, flexible, and designed for growth.

If you’re facing changes in your financing setup or rethinking your long-term strategy, I invite you to connect with the ChargeAfter team to see how we can help you move forward with confidence.

Ready to future-proof your POS financing?

About Kevin Lawrence

VP Global Lender Relations – Kevin has worked in the banking and finance industry for over a decade. He has worked closely with some of North America’s largest banks, financial institutions, and retailers. Kevin is an expert in embedded consumer financing and B2B financing. He has a deep understanding of current trends and where the industry is heading.