Category: R

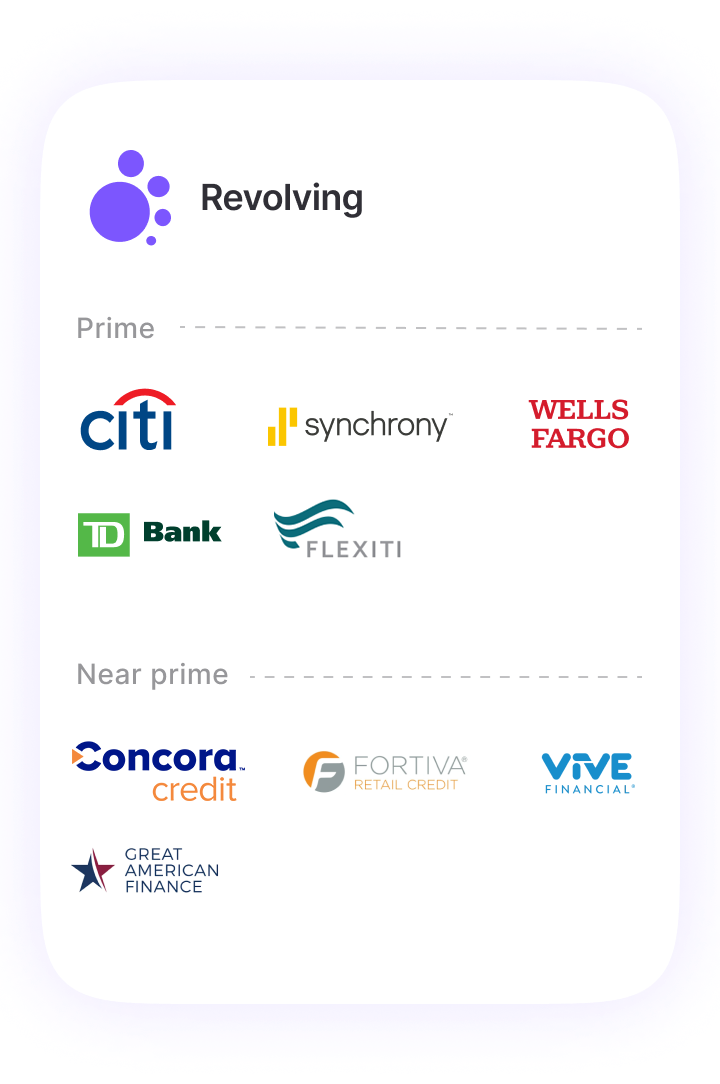

Revolving credit

What is a revolving credit?

Revolving credit, also known as revolving line of credit, is a flexible sales financing solution that allows consumers to borrow funds up to a specific limit and repay either at once or over time. Unlike a traditional loan, which provides a fixed amount of money upfront, a revolving credit line offers a pool of funds that can be tapped into repeatedly as long as the credit limit is not exceeded.

Benefits of revolving credit:

- Flexibility in borrowing: Consumers can draw funds as needed, making it an ideal solution for ongoing or unforeseen expenses.

- Reusability: After repaying the borrowed amount, the credit becomes available again, providing a continuous source of sales financing.

- Interest rates: Interest is only charged on the amount borrowed, not the entire credit limit, offering a cost-effective way to manage cash flow.

Limitations of revolving credit:

- Interest costs: Revolving credit often comes with higher interest rates compared to other forms of credit, leading to increased costs if balances are not paid in full, so is less suitable for certain types of shoppers.

- Administrative costs: Managing revolving credit programs involves administrative overhead, including account maintenance and monitoring customer creditworthiness. Merchants who want to serve all of their customers will need to offer more than a single revolving credit option, adding more costs and complexity.

- Regulatory compliance: Merchants must comply with regulations governing credit practices, adding complexity to operations and potential legal risks, especially when integrating multiple lenders.

To overcome these limitations, ChargeAfter’s embedded finance platform, enables merchants to seamlessly offer customer sales financing from multiple lenders that cover the entire credit spectrum and offer different types of financing options, while lowering administrative costs. In a single application, customers are matched with the best-fit financing choices in real time.